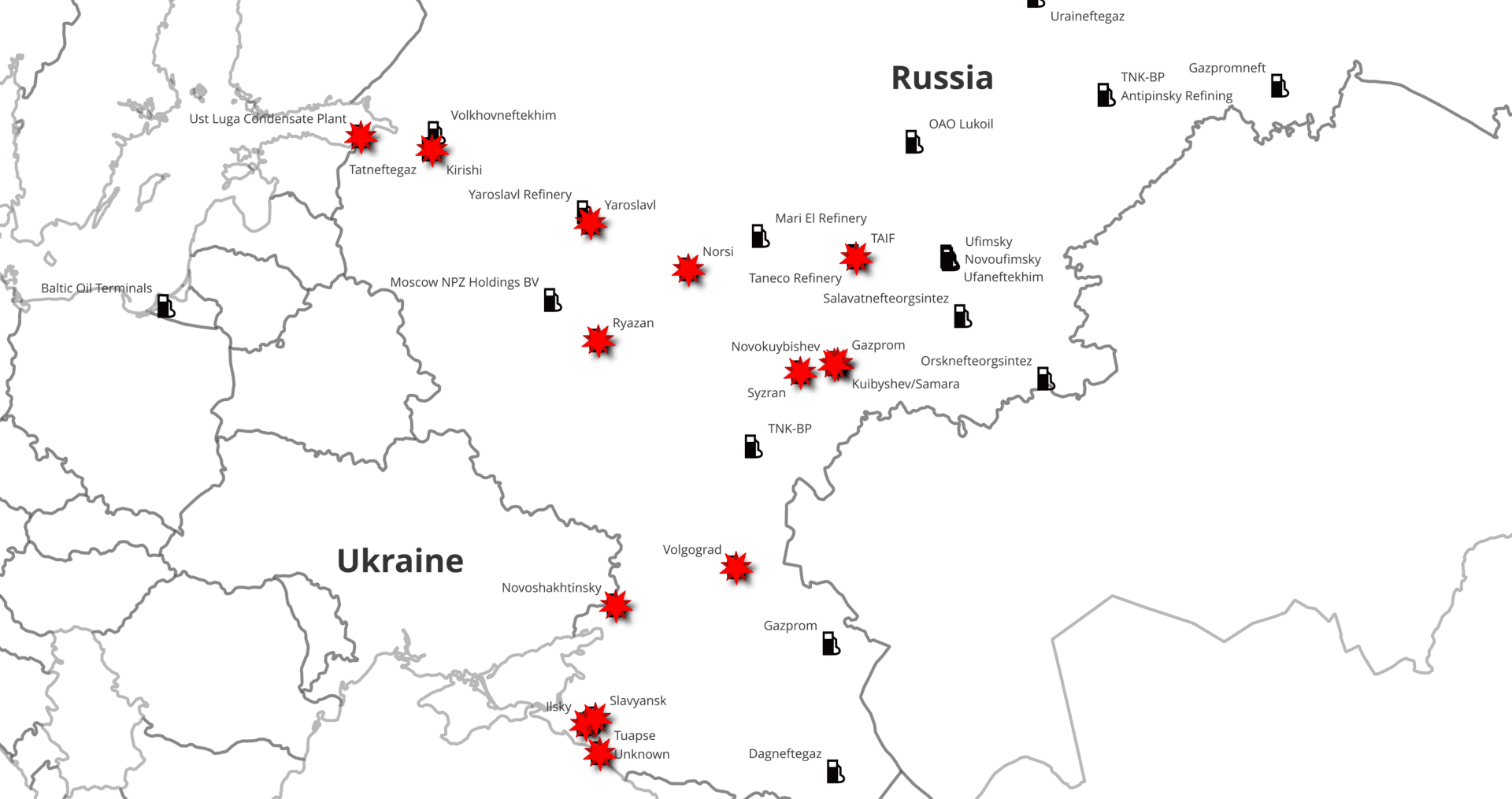

Since the start of 2024, Ukraine has intensified its attacks on Russian energy infrastructure, using one-way UAVs (suicide drones) to strike targets up to 700 miles from its border. Through April 2, 2024, 14 refineries and 9 crude and product terminals have been targeted and damaged. Russia holds nearly 7 million barrels per day (mbd) of nameplate refining capacity, of which the EIA estimates 5.5 mbd is operable. The targeted refineries account for close to 3.34 mbd of capacity, an estimated 1.3 mbd of which has been impaired. Of these, three produce primarily for export and three serve both export and domestic markets, together representing 1.2 mbd.

Tariffs on Russian crude and product exports are central to funding the national treasury and the war effort. Year-on-year, Russian monthly product exports are estimated to be down 1 mbd in March 2024, from 3.0 mbd in March 2023. The refining constraints prompted Russia to ban gasoline exports beginning March 1, 2024, and to begin importing gasoline from Belarus.

The market impact abroad appears contained. European product markets have been tight since Russia escalated its aggression in February 2022, and any effect from the drop in Russian exports is expected to be minimal. The U.S. relies on roughly 1+ mbd of gross product imports, mostly from Canada; substantial Russian product imports that persisted until December 2022 have since been replaced by supply from Venezuela.

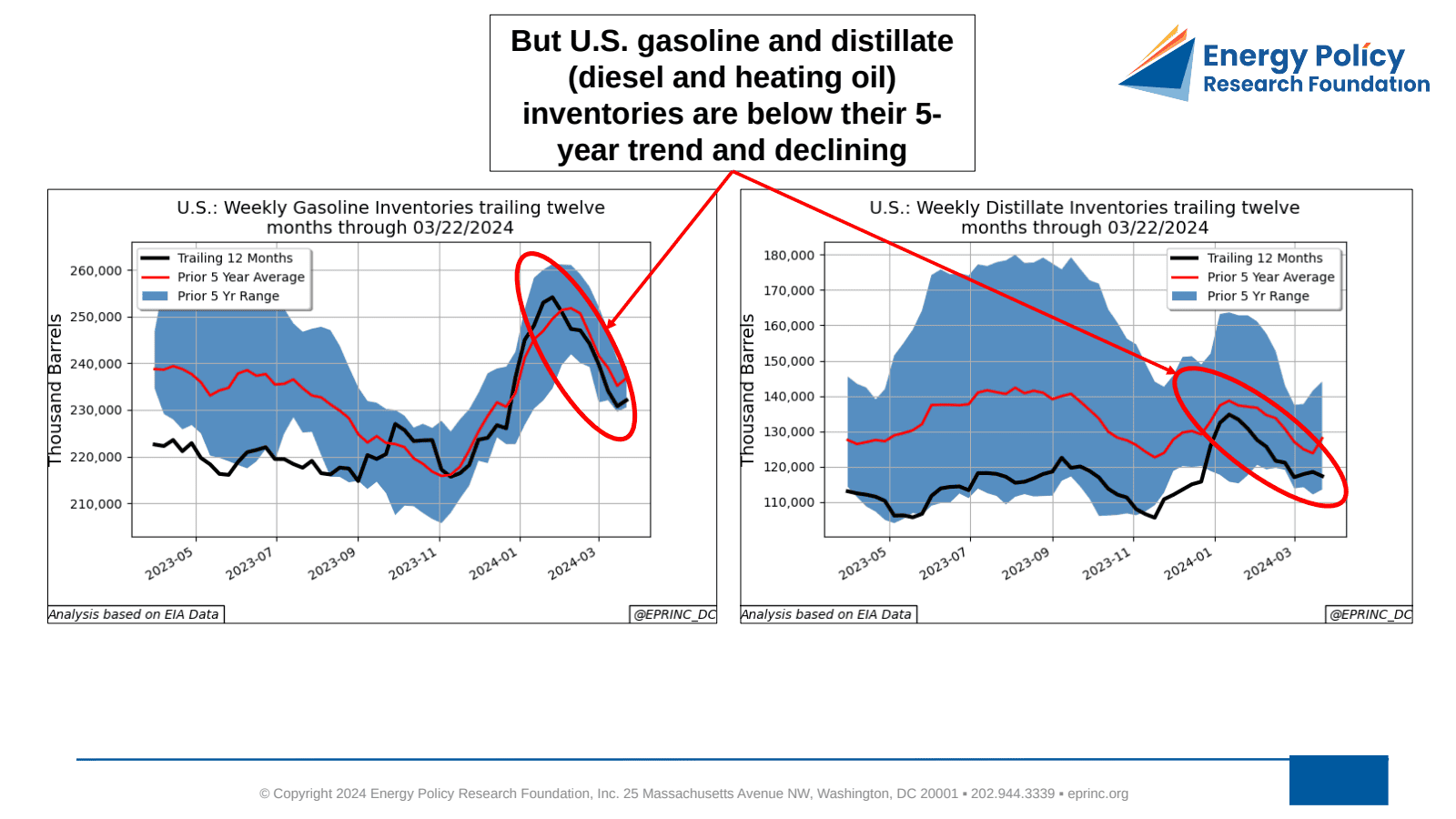

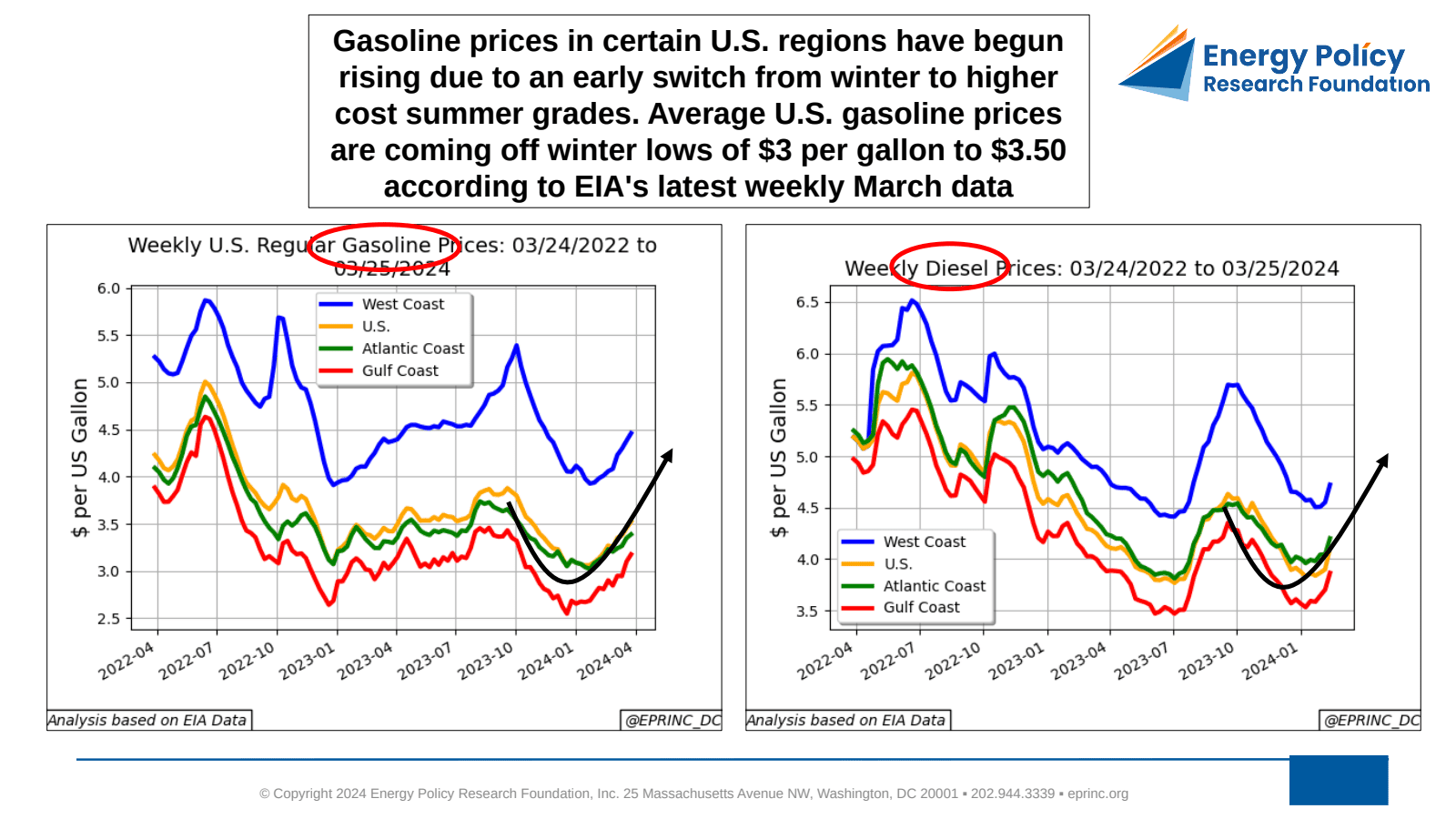

Domestic conditions are nonetheless tightening. U.S. refining utilization has risen to nearly 90% from a winter low of 80%, while gasoline and distillate inventories sit below their five-year trend and are declining. Gasoline prices in some regions have begun rising with an early switch to higher-cost summer grades, with average U.S. prices coming off winter lows of $3.00 to $3.50 per gallon in EIA’s latest weekly March data. Current markets show none of the price spikes or volatility seen in 2022, but media reports indicate the Biden administration is concerned that continuing attacks could drive up global prices.

“Rising transportation fuel price wariness is one of the most durable issues in the U.S. political space, especially during an election year,” said Max Pyziur, EPRINC’s Research Director. “But Russia’s product export reduction in response to damaged refining capacity coupled with ongoing Red Sea shipping threats do not appear to be abating soon. Combined with a tightening U.S. situation, these are providing a solid floor for prices. In the event of a major price spike, policy maneuvers could be limited.”

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Ukrainian Strikes on Russian Refineries and Global and U.S. Product Markets,” Chart of the Week 2024-13, March 25, 2024.