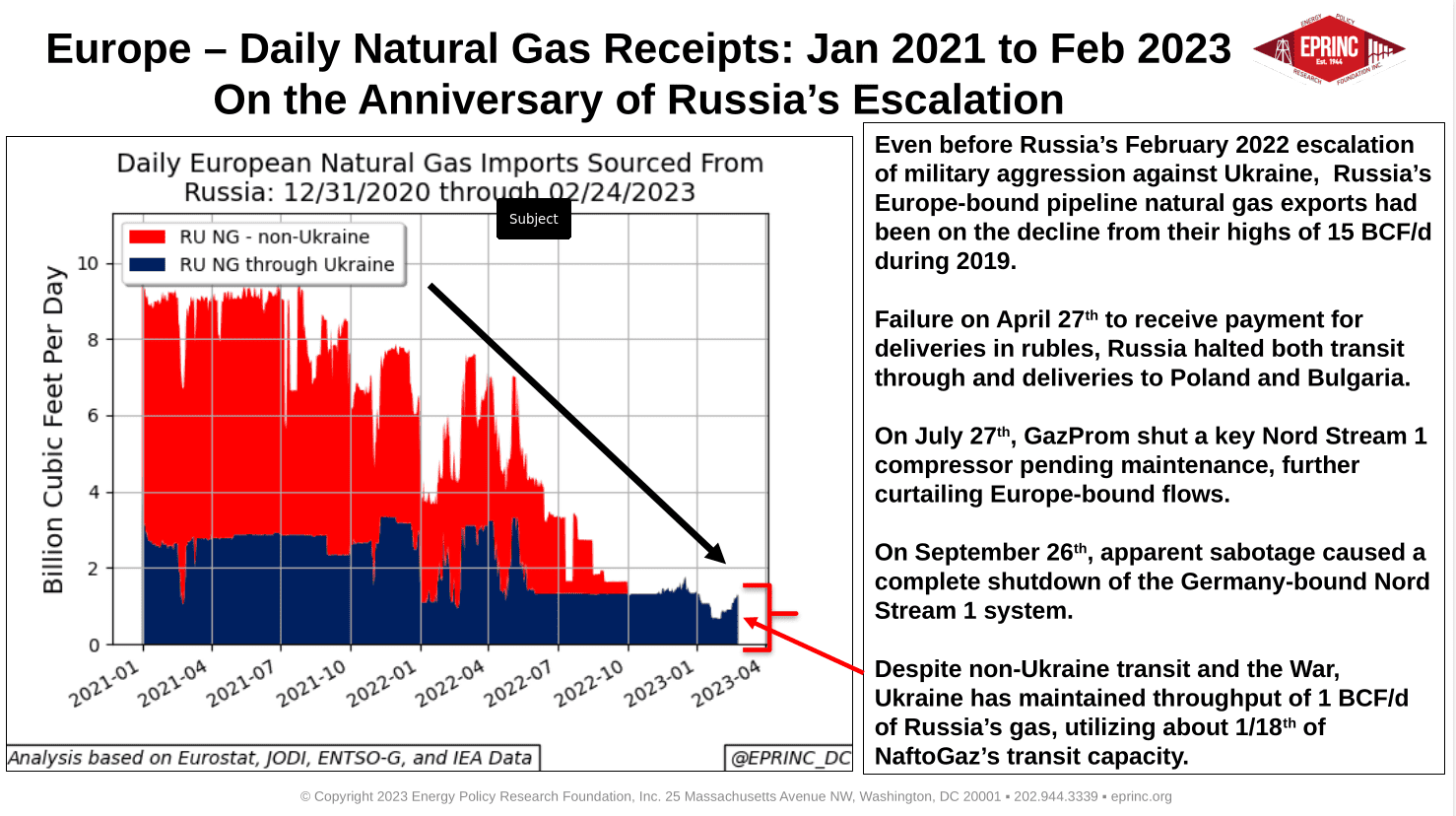

The chart tracks daily natural gas receipts into Europe from January 2021 through February 2023, capturing the shift in supply sources across the first year of Russia’s escalated aggression against Ukraine. Russia’s Europe-bound pipeline exports had already been declining from their 2019 highs of 15 BCF/d, and a series of 2022 disruptions accelerated the change: Russia halted transit and deliveries to Poland and Bulgaria on April 27th after payment was not made in rubles, Gazprom shut a key Nord Stream 1 compressor for maintenance on July 27th, and apparent sabotage caused a complete shutdown of the Germany-bound Nord Stream 1 system on September 26th.

Despite early fears when the escalation began, there were no sustained sizeable physical disruptions. Aggressive replenishment of inventories combined with a mild winter mitigated the potential severity and costs. European buyers moved quickly to secure alternatives: Poland’s PGNiG, the U.K.’s Ineos, France’s Engie, and others signed an additional 2 BCF/d in long-term U.S. LNG contracts for deliveries between 2023 and 2026, while Italy was the most active in diversifying away from Russian gas, signing or strengthening procurement agreements with ten countries including Qatar, Azerbaijan, Egypt, and the U.A.E. Even Ukraine has maintained throughput of about 1 BCF/d of Russian gas, roughly one-eighteenth of Naftogaz’s transit capacity.

Europe’s response has so far been tactical rather than strategic. The war has driven a long-term restructuring of trade flows, particularly for LNG. Forecasters expect European LNG requirements to rise from the 10 BCF/d that prevailed over the prior five years to a range of 17 to 20 BCF/d, which will demand significant infrastructure and planning. Germany has begun to repurpose existing infrastructure with floating storage and regasification units (FSRUs) and to build new facilities, but other potentially large LNG-consuming European countries have not yet begun to act.

The outlook is complicated by global demand. If East Asian consumers such as China and Japan revert to using more LNG, and as new demand emerges from South and Southeast Asia, global LNG markets are set to tighten considerably unless new liquefaction plants are commissioned.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “On the Anniversary of Russia’s Escalation,” Chart of the Week 2023-09, February 27, 2023.