Lithium is the critical mineral required for most utility-scale power storage, electric vehicle batteries, and the batteries in smartphones and laptop computers. Because it is unstable in its pure elemental form, lithium is marketed as one of two compounds: lithium hydroxide, in which lithium is 29% of total mass, or lithium carbonate, in which it is 18.8%. Over the past few years, prices for both compounds have risen considerably as demand has outpaced supply.

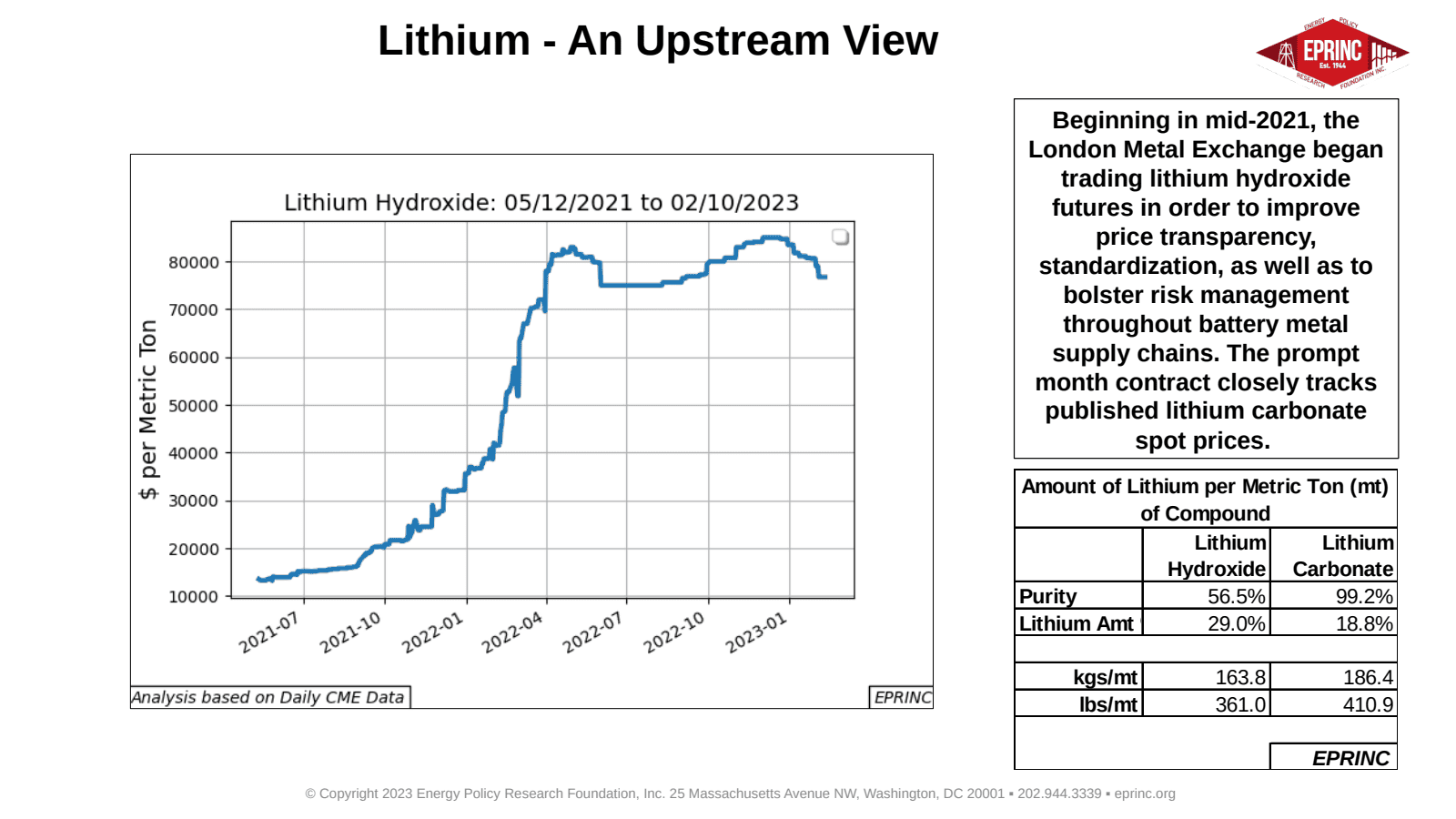

Allkem (formerly Orocobre) and Sociedad Quimica y Minera (SQM) are two of several producers operating in the “lithium triangle,” a prolific lithium-producing region straddling the borders of Chile, Argentina, and Bolivia. SQM, a Chilean-based major, is estimated to produce about 16% of total global supply. Allkem, a junior headquartered in Brisbane, Australia, produces about 4% of global supply, with its primary operations in the Olaroz formation in northern Argentina. Beginning in mid-2021, the London Metal Exchange began trading lithium hydroxide futures to improve price transparency, standardization, and risk management across battery metal supply chains; the prompt month contract closely tracks published lithium carbonate spot prices.

A Tesla Model S with a 70 kWh battery requires 63 kilograms (138 pounds) of lithium carbonate-equivalent (LCE), or 11.8 kilograms (26 pounds) of pure lithium, so one metric ton of LCE covers the lithium requirements of nearly 16 such batteries. Based on an average of Allkem and SQM prices, the LCE cost for one Tesla Model S rose from an average of $972 in the third quarter of 2018 to $3,112 in the third quarter of 2022.

LCE demand was estimated at 564 thousand metric tons in 2021. For 2030, the International Energy Agency (IEA) forecasts almost 1.4 million metric tons of LCE primary demand under its Stated Policies Scenario and over 2.5 million metric tons under its Sustainable Development Scenario. Reaching those levels would require lithium production to grow at an annualized rate of 10.6% in the former case and 18% in the latter.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Lithium – An Upstream View,” Chart of the Week 2023-08, February 20, 2023.