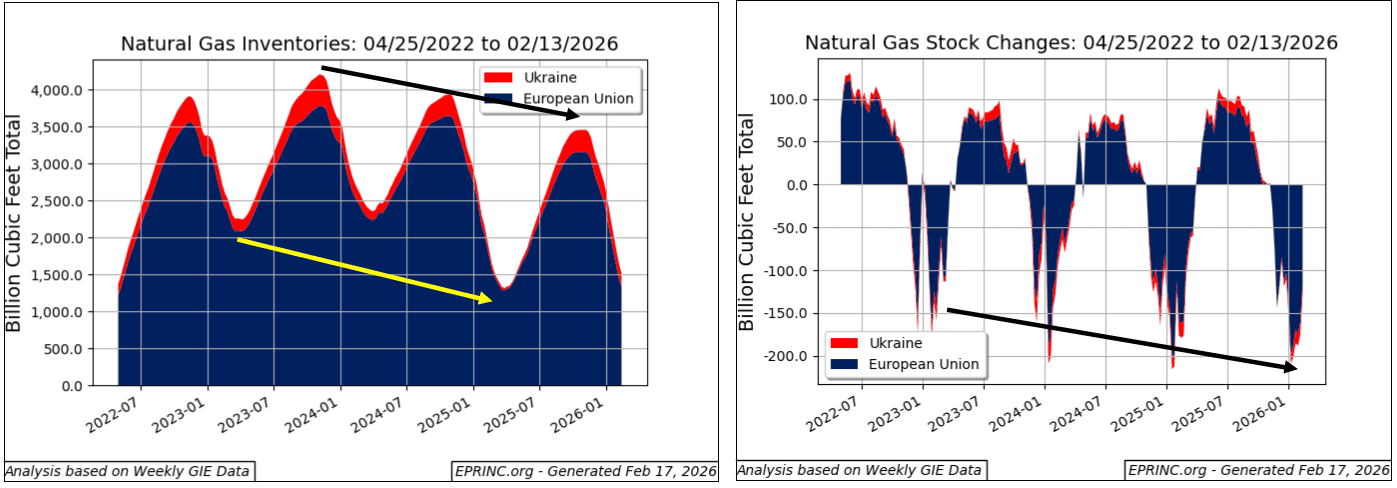

Recent winters across the northern latitudes have been harsh, elevating reliance on natural gas for additional seasonal power and heating in both the United States and Europe. Europe and Ukraine hold a combined 5 trillion cubic feet (tcf) of storage capacity — 4 tcf in Europe and 1 tcf in Ukraine. In recent years Ukraine’s storage has been used to support the rest of Europe, but Russia’s military aggression has curtailed its utilization to half.

Mid-year European natural gas replenishments peaked in November 2023 at 4.2 tcf (3.8 tcf in Europe and 0.42 tcf in Ukraine) and have not attained similar levels since. Winter inventory depletions are on track to continue reaching new lows, requiring more aggressive replenishments.

European sanctions policy against Russia, the failure to renew pipeline transit agreements, and related developments have shifted Europe from a situation in which most natural gas imports arrived via international pipelines to one in which the majority now moves as LNG. Since mid-2022, the bulk of that Europe-bound LNG has come from the United States.

Despite this change in strategy, total European natural gas imports have trended lower.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “European Natural Gas Inventories A Late 2025-2026 Winter Assessment,” Chart of the Week 2026-07, February 9, 2026.