A curtailment of 10% of U.S. natural gas production would lead to a reduction of 10.5 BCF/d from a total of 110.5 BCF/d, of which 1.5 would be from associated fields. That in turn would lead to a curtailment of 425 TB/d of crude oil, or 3.6% of total U.S. crude oil production.

NGLs would be impacted similarly since 90% of NGL production is tied to that of natural gas.

In a 2014 peer-reviewed Energy Strategy Reviews article, “The Global Gas Market, LNG Exports, and the Shifting U.S. Geopolitical Presence,” respected energy policy researchers Amy Myers Jaffe, Meghan O’Sullivan, and Kenneth Medlock wrote:

“Of particular debate is whether the United States government should undertake policies to promote exports of liquefied natural gas (LNG) from its shores in the wake of the Russian-Ukraine conflict of the spring of 2014. Recent political rhetoric has even suggested that the United States could replace Russia as the major supplier of natural gas to Europe or somehow use trade policy to favor allied nations, especially North Atlantic Treaty Organization (NATO) members, in the process of granting export licenses to natural gas companies seeking to export U.S. LNG.

“The prospects that Russia could further use its natural gas exports as a geopolitical lever has elevated strategic elements of U.S. natural gas policy and intensified interest in a push to increase U.S. presence in the global gas market. While the level of U.S. exports will ultimately rest on the commercial decisions of energy companies, U.S. and European governments, through policy, can remove barriers to commercial opportunities and even promote trade flows otherwise not deemed to be commercial.”

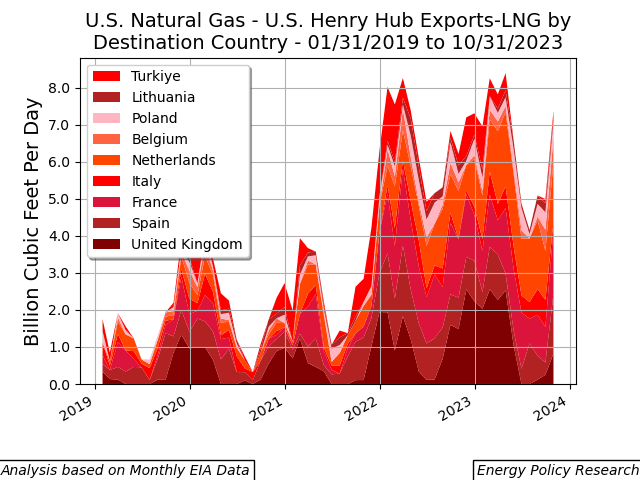

As a result of the application of new technologies to hydrocarbon development, natural gas production has grown faster than consumption, and the U.S. has been able to shift to an exporter, moving natural gas via pipelines and LNG tankers. In 2022, U.S. gross natural gas exports averaged 18.8 billion cubic feet per day (BCF/d), of which 10.6 were in the form of LNG, and of which 5 to 8 BCF/d of the LNG were exported to Europe (please see Figure 1).

As Lucian Pugliaresi, EPRINC’s President, along with Fred Hutchinson, President of LNG Allies, wrote in a recent OpEd:

“This has transformed our domestic energy situation—enabling vast renewable power growth, significant coal-to-gas switching, large CO2 reductions, and the reshoring of dozens of fertilizer, chemical, and other industrial facilities. It has also made America the top LNG exporter and permitted us to bolster the energy security of allied nations from Japan and Korea to Poland and Germany.

“U.S. LNG exports are making substantial contributions to U.S. trade balances and domestic employment and bolstering the energy security of our allies. The disruption of pipeline gas shipments to Europe following the Russian invasion of Ukraine was a severe blow to European economic growth and security.

“Alliance cohesion in response to the Russian invasion of Ukraine would be much more difficult in the absence of U.S. LNG, and although some in Europe initially viewed such shipments as a temporary necessity, a more pragmatic view is emerging.”

U.S. European allies are underscoring the importance of this alliance. “Since March 2022 [a few weeks after Russia’s invasion of Ukraine], U.S. developers have signed 57 supply agreements representing about 73 million metric tons of LNG annually [9.5 BCF/d] … more than four times the number of contracts they signed between 2020 and 2021,” reported Benoît Morenne in the Wall Street Journal.

Information on these charts is available at: https://eprinc.org/chart-of-the-week/

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Unintended Consequences Of Curtailments Of USNatural Gas Production,” Chart of the Week 2024-03, January 15, 2024.