With the conflict in its third week, most attention has centered on restoring the 18.6 MB/d of crude oil that transits the Strait of Hormuz. Some pipeline transit has been rerouted to the Red Sea, and the International Energy Agency has announced a coordinated release of 400 million barrels over the next 120 days to ease shortages. Far less attention has fallen on the 10.6 BCF/d of LNG that also moves through the strait, of which 10.3 BCF/d originates in Qatar.

On March 11, 2026, Qatari LNG production was curtailed after numerous shipping customers declared force majeure, unable to transit Hormuz. Qatari LNG production and exports were subsequently halted. Qatar accounts for almost 20% of the world’s 52.6 BCF/d of LNG exports, making the loss material to the global market.

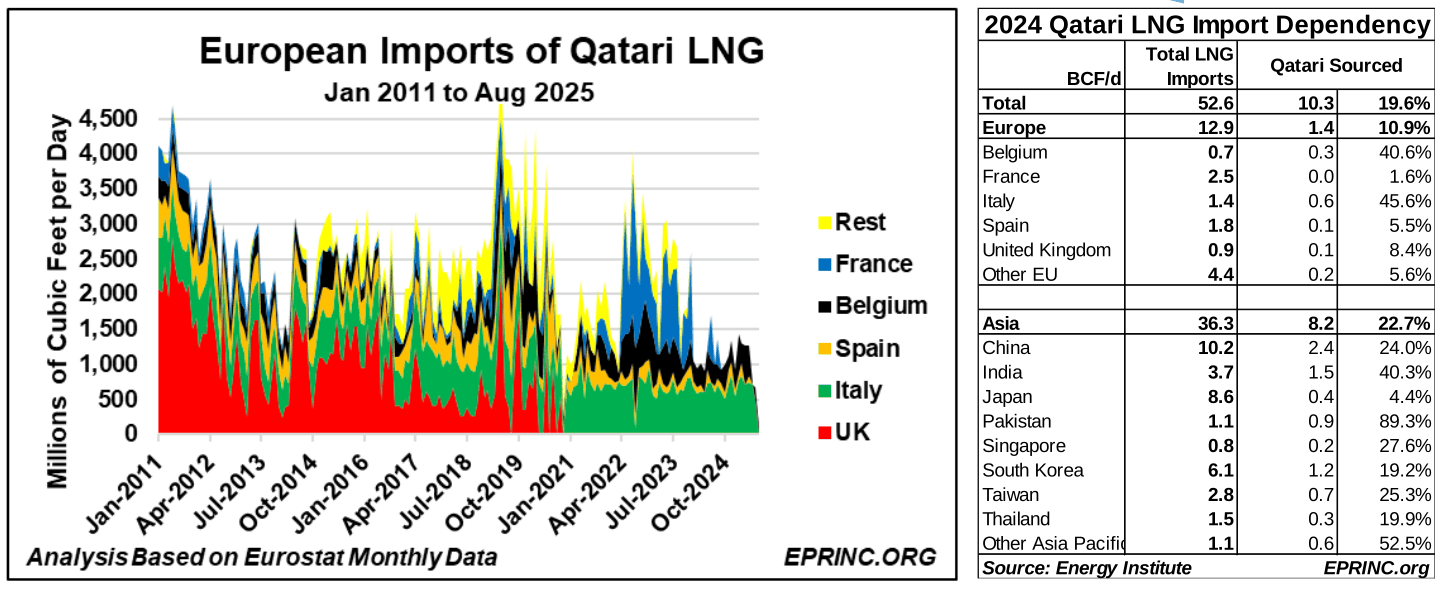

The exposure is uneven across regions. European reliance on Qatari LNG is limited in aggregate: of 12.9 BCF/d of average 2024 European LNG imports, 1.4 BCF/d (11%) came from Qatar, and Europe has shifted markedly toward U.S. supply since 2011, when it imported over 4 BCF/d of Qatari LNG. Even so, Belgium and Italy each depend on Qatar for more than 40% of their LNG imports.

Asian importers carry the greater dependency. Of 36.3 BCF/d imported into the region, 8.2 BCF/d (22.7%) comes from Qatar, with China, India, and Korea together requiring 5.1 BCF/d, representing 20-40% of each country’s LNG needs. A prolonged closure would therefore concentrate its sharpest effects on Asian buyers and on the most Qatar-dependent European markets.

For more information on these charts, please contact Max Pyziur (maxp@eprinc.org).

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Strait of Hormuz Closure: Qatari LNG Curtailment and the Global Gas Market,” Chart of the Week 2026-11, March 9, 2026.