Beginning in early 2021, Russia engaged in a strategic reduction of its pipelined natural gas exports. Through a series of reciprocating steps that culminated in the severe curtailment of pipeline flows across all transit capacity available to Russia, Europe’s imports of Russian natural gas fell to less than 1 BCF/d (billion cubic feet per day) by the summer of 2022, down from a high of 15 BCF/d in 2019.

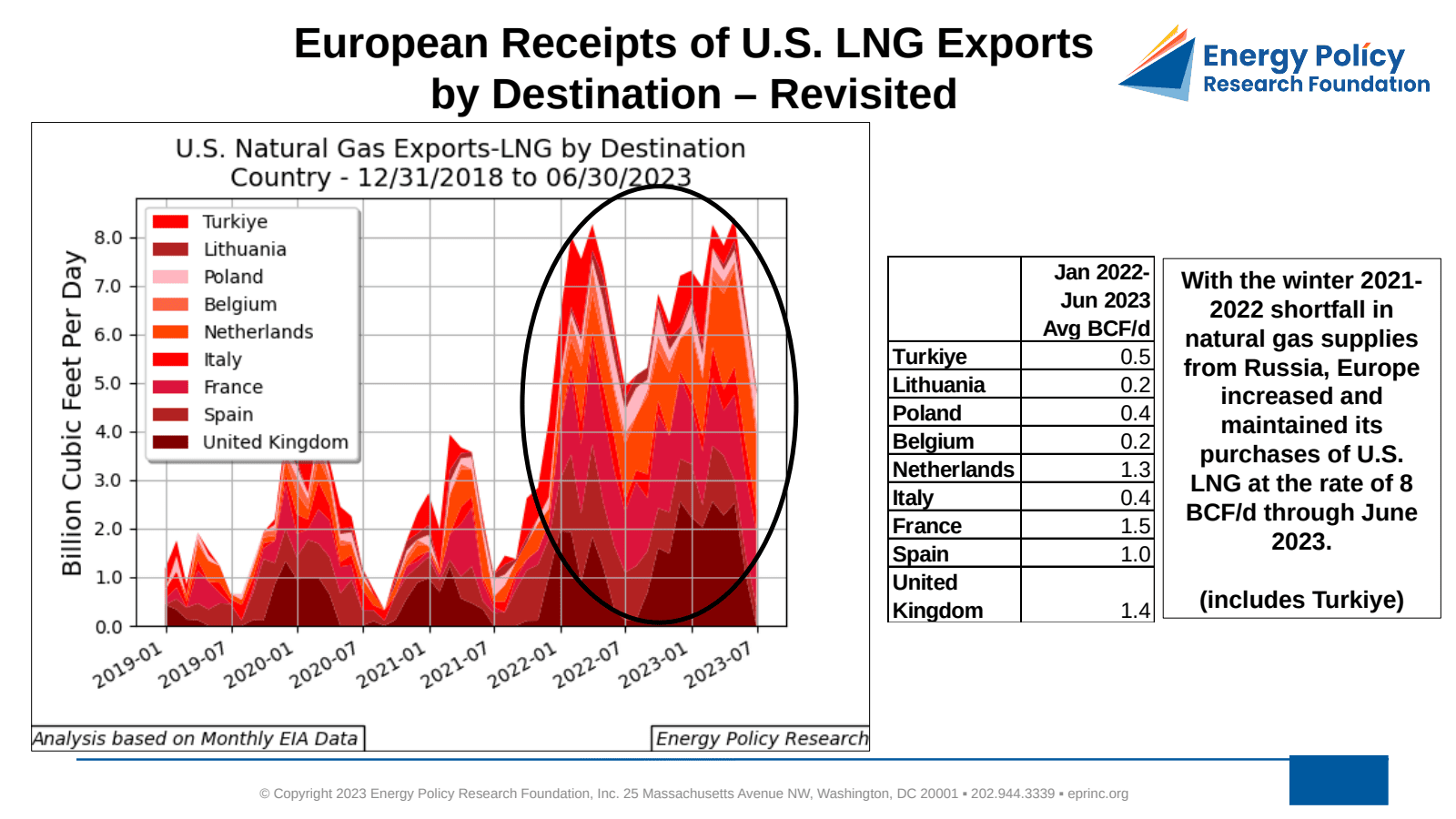

In response to this degradation of Russian supply, Europe expanded its natural gas imports from other sources, most notably U.S. LNG (liquefied natural gas). The chart tracks European receipts of U.S. LNG exports by destination on a quarterly basis. Beginning in January 2022, European U.S. LNG imports increased from 2 BCF/d to almost 8 BCF/d—roughly 50% of Europe’s LNG requirements. This elevated level has continued into 2023.

According to Max Pyziur, EPRINC’s Research Director, alliance cohesion in response to Russia’s invasion of Ukraine and the commercial availability of U.S. LNG exports have been vital. Without these fuels, he noted, Europe’s 2022–2023 winter would have been bleak, and until other resources become available, it remains critically important that these imports continue.

EPRINC President Lucian Pugliaresi and LNG Allies CEO Fred Hutchison recently authored “Streamline the Regulatory Process to Expedite U.S. LNG Exports,” published by RealClear Energy, calling for simplification of the U.S. LNG export regulatory process. Existing applications, especially those to non-FTA countries, once processed in a timely manner, have been delayed considerably since the first major U.S. LNG exports sailed from the U.S. Gulf Coast.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “European Receipts of U.S. LNG Exports by Destination – Revisited,” Chart of the Week 2023-42, October 16, 2023.