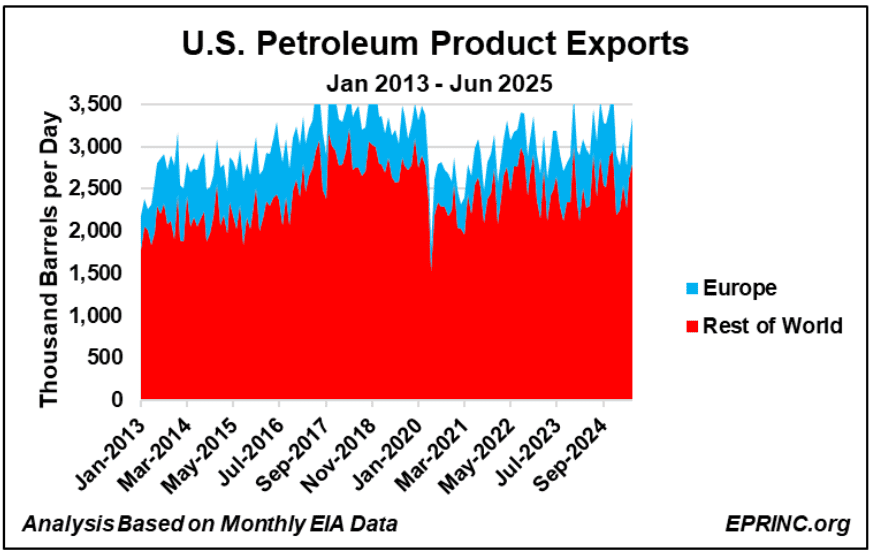

With refining capacity of approximately 18 million barrels per day (MB/d), the U.S. refinery fleet supplies the domestic market abundantly while also generating sizeable petroleum product exports—gasoline, jet fuel, distillate, and heavy fuel oil. Over the past ten years, these product exports have averaged almost 3.1 MB/d.

On July 28, 2025, the Trump administration concluded a nonbinding framework agreement for the EU to purchase $750 billion of U.S. energy over three years ($250 billion per year), a total that would include imports of U.S. petroleum products.

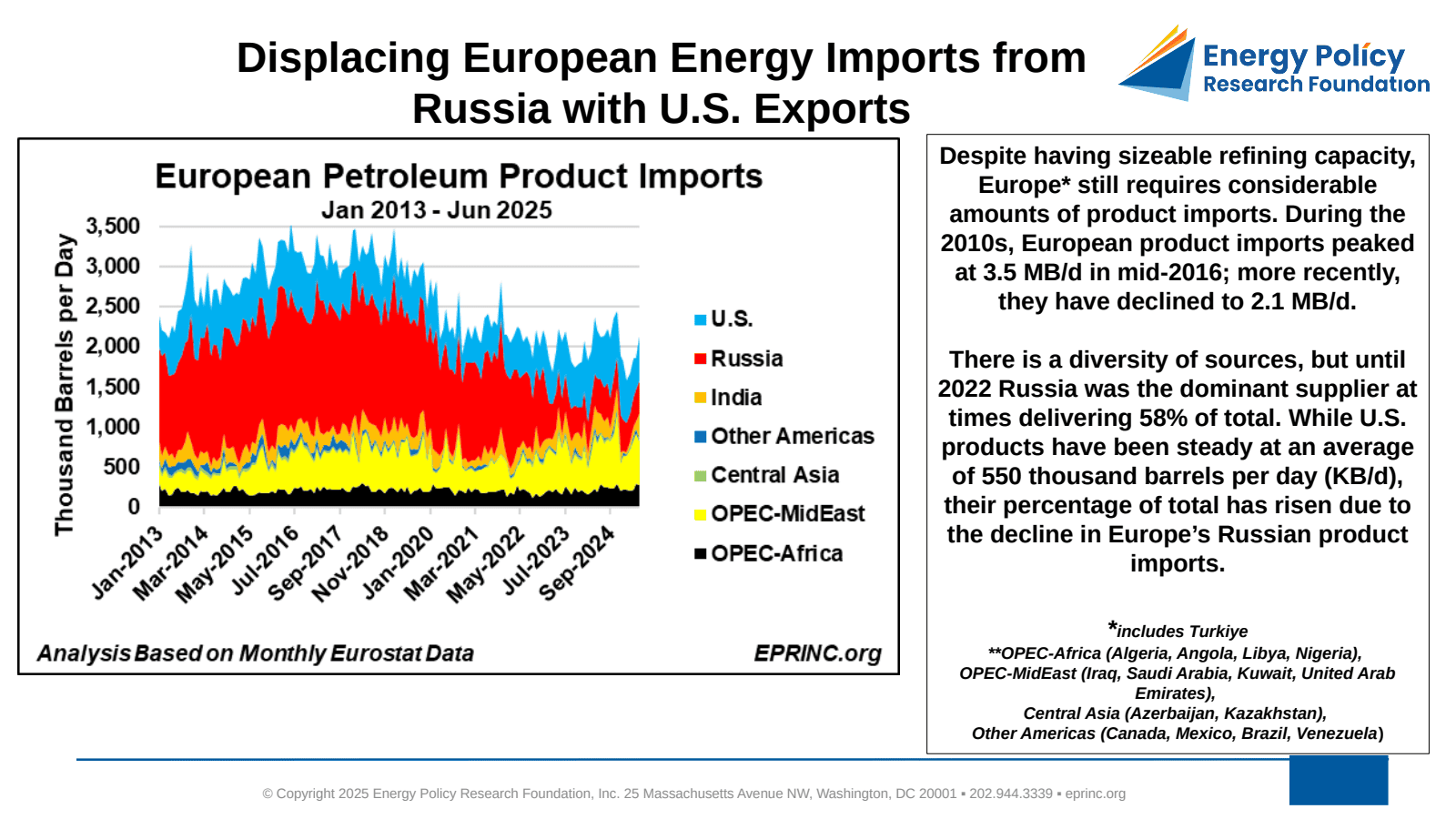

Despite its own sizeable refining capacity, Europe still requires considerable product imports. These peaked at 3.5 MB/d in mid-2016 before declining more recently to 2.1 MB/d. Supply sources are diverse, but until 2022 Russia was the dominant supplier, at times delivering 58% of the total. U.S. products have held steady at an average of 550 thousand barrels per day (KB/d), and their share of the total has risen as Russian product imports have fallen.

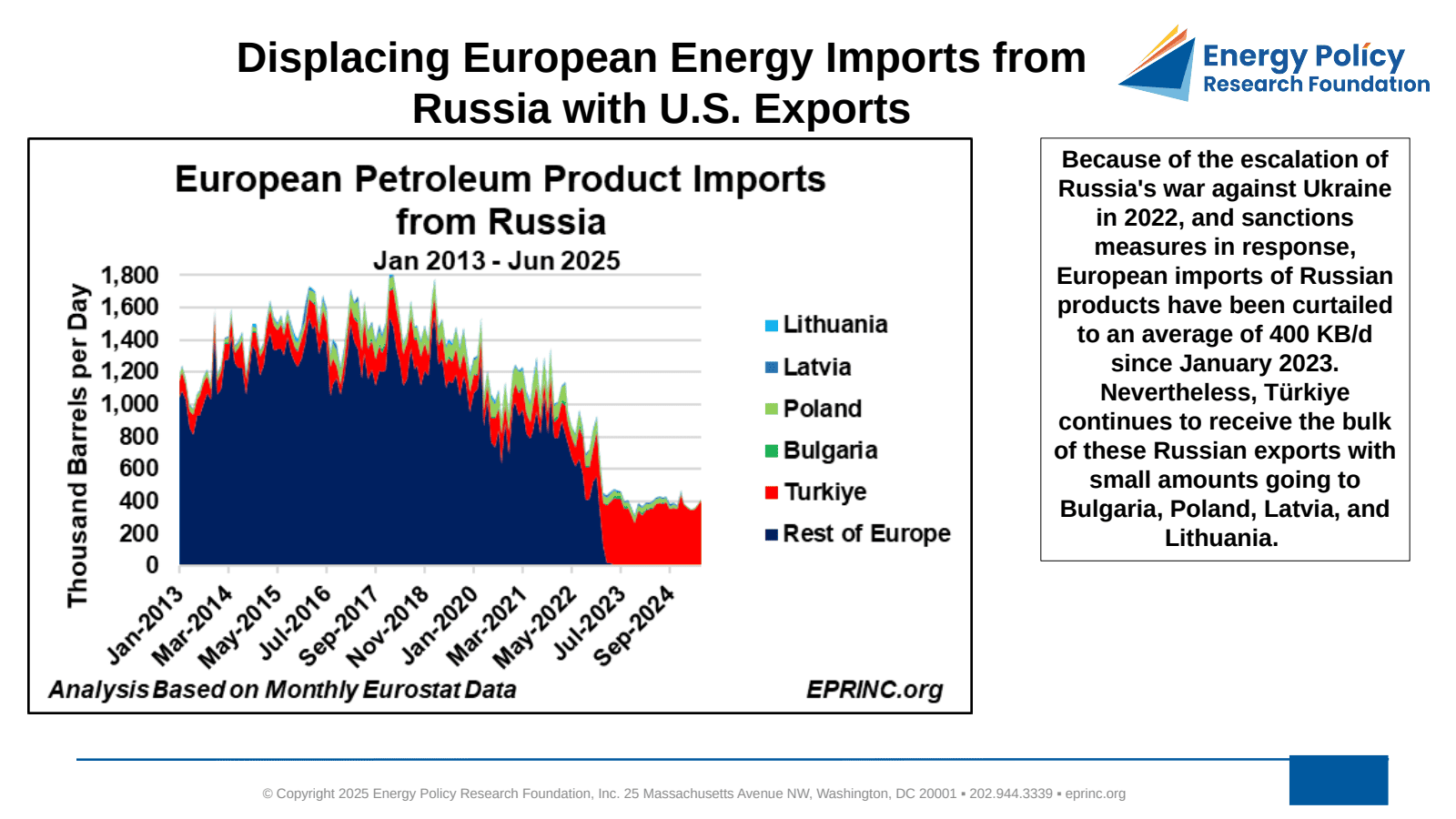

Following the escalation of Russia’s war against Ukraine in 2022 and the sanctions imposed in response, European imports of Russian products have been curtailed to an average of 400 KB/d since January 2023. Türkiye continues to receive the bulk of these Russian exports, with small amounts going to Bulgaria, Poland, Latvia, and Lithuania.

Over the past four years, the total value of U.S. product exports has averaged approximately $114 billion per year, of which about $19 billion (roughly 16.5%) has been delivered to Europe. EPRINC’s analysis extends beyond the 27 EU member states to include Türkiye and the United Kingdom. A companion analysis assessed Displacing European Energy Imports from Russia with U.S. Exports — the Case of Crude Oil.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Displacing European Energy Imports from Russia with U.S. Exports – The Case of Petroleum Products,” Chart of the Week 2025-37, September 8, 2025.