The Dallas Federal Reserve Bank regularly surveys U.S. crude oil and natural gas producers in its jurisdiction, an important economic sector in its district. Reports of the data gleaned from these surveys are published quarterly (https://www.dallasfed.org/research/surveys/des/2025/2501). One key set of metrics is producers’ price level requirements for operations and profitability.

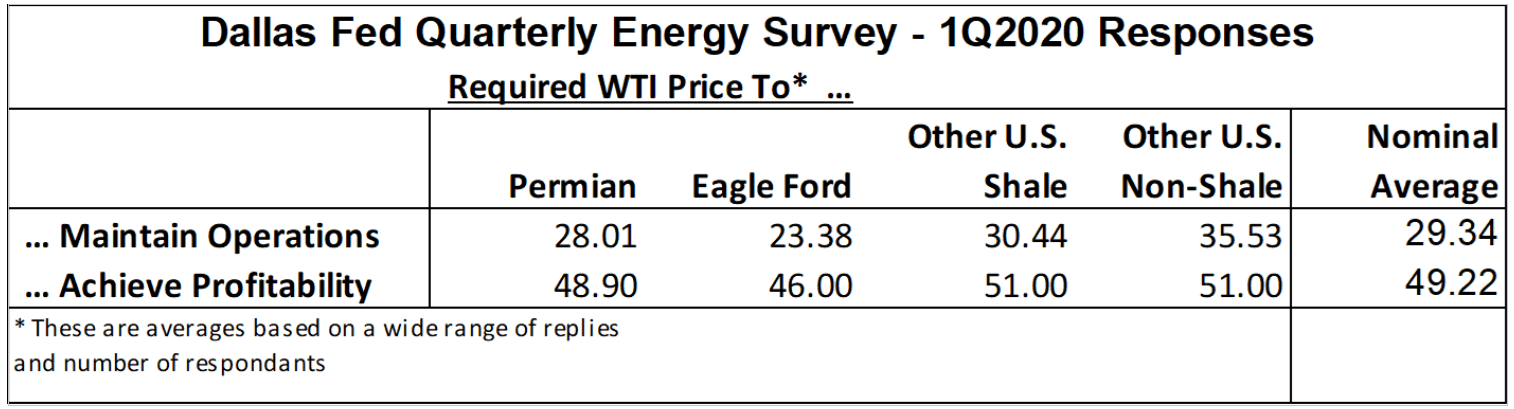

Results vary by producing region, with the Permian being the largest by far. Nominal averages are provided in the tables. Viewing first respondents’ answers from the first quarter of 2020, just ahead of the COVID-19 Pandemic, the average required WTI (West Texas Intermediate crude oil benchmark price) to maintain U.S. operations was just over $29/bbl (per barrel). For profitability, the average response came in at $49/bbl (Table 1).

The first quarter 2025 survey showed significantly higher results reflecting general inflationary trends. The average breakeven WTI price was reported at $39/bbl; the average WTI price required for profitability was almost $64/bbl (Table 2).

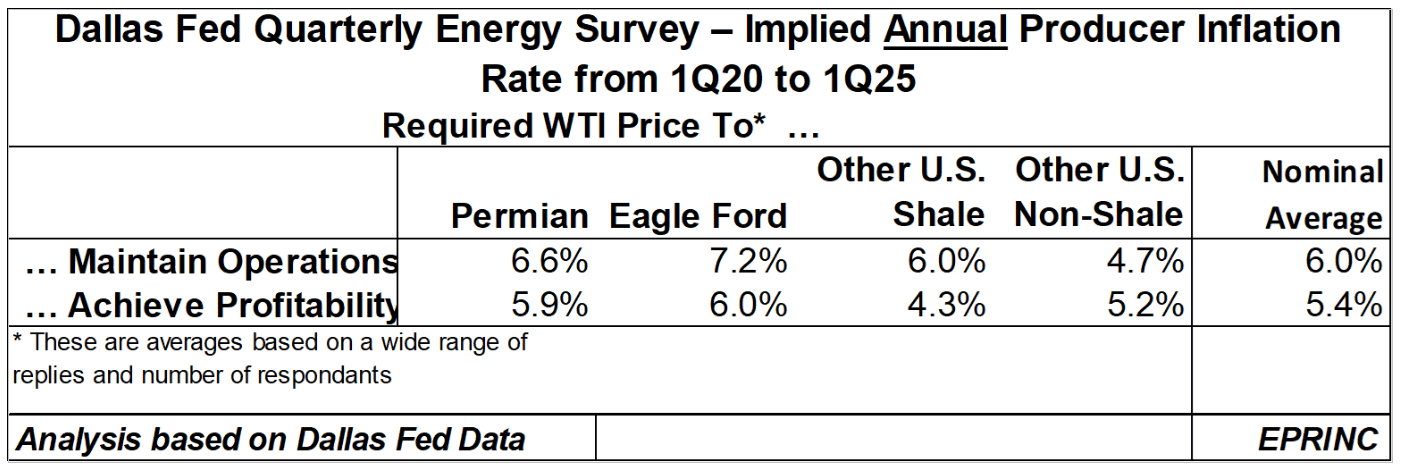

Using data from these two surveys, the implied annualized producer inflation rate for “maintain operations” is 6% and for profitability is 5.4% (Table 3).

After declining from their early 2022 peaks, WTI prices have been range-bound since November 2022, fluctuating between the $60s and the low $90s.

“But recent volatility and sharp declines due to a combination of economic slowing and enacted high U.S. tariff policies have pushed prices to $60/bbl,” said Max Pyziur, EPRINC’s Research Director. “If respondents are faithful in their replies to the Dallas Fed’s survey, the current WTI price environment will lead to a degradation in U.S. crude oil and natural gas production, contrary to stated policies of President Trump’s administration.”

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Dallas Fed Survey: U.S. Crude Oil Production Costs Are Rising – Revisited,” Chart of the Week 2025-14, March 31, 2025.