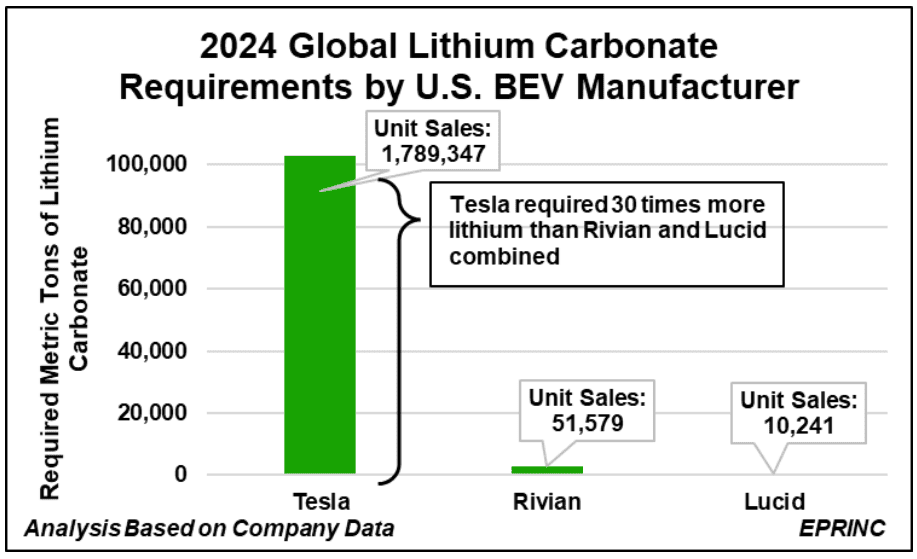

Battery electric vehicles are lithium-intensive: each requires roughly 11 kilograms (24.25 lbs) of lithium, sourced from about 63.5 kilograms (140 lbs) of lithium carbonate equivalent (LCE) for its battery. This chart translates the 2024 global sales of the three BEV-only U.S. manufacturers—Tesla, Rivian, and Lucid—into their corresponding annual lithium requirements.

Tesla dominates the group. With 2024 global sales of 1.8 million vehicles, it far surpasses Rivian’s 51,500 units and Lucid’s 10,200 units. Tesla’s batteries require approximately 113,600 metric tons of LCE (21,200 metric tons of lithium) annually, just over 11% of global production. That figure exceeds the combined needs of Rivian (3,300 metric tons of LCE) and Lucid (650 metric tons) by nearly 30 times.

Global supply is concentrated. Chile and Australia, the top two producing countries, together account for 72% of production, followed by China at 17%. The United States accounts for just 0.3%.

Domestic supply constraints are notable given the scale of this demand. The United States holds 25.6 million tons of combined LCE reserves and resources, yet current production comes entirely from one small Nevada mine. Five additional U.S. mining locations are in various early stages of permitting. Bringing a lithium mine into production in the United States can take up to 28 years, compared with ten to fifteen years in countries such as Ghana or the Democratic Republic of the Congo.

Because elemental lithium is unstable, it is marketed in compound forms—most frequently as lithium carbonate and lithium hydroxide, with lithium purity of 18.6% and 16.4%, respectively.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Global Lithium Requirements of Select U.S. BEV Manufacturers,” Chart of the Week 2025-15, April 7, 2025.