“Until just a few years ago, the use of utility-scale battery storage was not apparent,” said Max Pyziur, EPRINC’s Research Director. “But some combination of Renewable Portfolio Standards coupled with commercial and operational needs such as frequency regulation, price arbitrage across periods throughout the day, and storage of excess wind and solar power generation have driven its development rapidly (https://www.eia.gov/todayinenergy/detail.php?id=50176).”

Growth: U.S. utility-scale battery storage systems have grown rapidly to 20,710 megawatts (MWs) in 2024 from 1,570 MWs in 2020; annualized, this is a rate of 90.6%. Through 2030, plans are in place for U.S. utility-scale battery systems to expand to 30,500 MWs (16.3% yearly) (Figure 1).

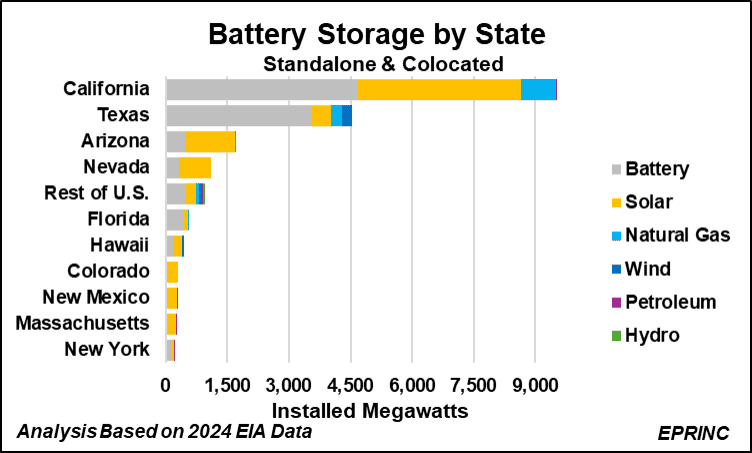

California and Texas dominate battery adoption, accounting for 47.9% (9,900 MWs) and 23.3% (4,800 MWs), respectively. However, if current system expansion plans are executed, Texas will increase its installed capacity to 19,350 MWs in 2030, surpassing California’s projected increase to 15,110 MWs. In addition, Arizona and Nevada have developed significant battery storage systems of 1,700 MWs and 1,100 MWs, respectively.

Siting/colocation: California distinguishes itself with having over 50% of its battery systems collocated (sited) adjacent to other power systems, primarily solar facilities (42%) and to a lesser degree natural gas-fired generators (8.3%). Battery systems in Texas are primarily standalone (78.7%), with the balance collocated with solar, natural gas, and wind systems (Figure 2).

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “U.S. Utility-Scale Battery Storage Developments,” Chart of the Week 2024-44, October 28, 2024.