On February 1, 2025, President Donald Trump issued a set of three Executive Orders (EOs) applying tariffs to all imported goods from Canada, Mexico, and China. They were scheduled to go into effect on February 4, 2025, lasting indefinitely until a time when the president would decide to remove them. Additional tariffs would be levied depending on the nature of retaliatory actions. The key rationale across all three EOs is to take punitive action against the flow of illegal drugs and their components from Mexico, Canada, and China.

Rather than immediately engage in a tariff war, Canada and Mexico made provisional adjustments in border controls. In response, President Trump’s administration postponed enacting tariffs on Canada and Mexico for thirty days pending other developments.

The tariffs were pegged at a rate of 25% on the value of imported goods from Mexico and Canada, and 10% from China. The key exception was that tariffs on imports of Canadian “energy and energy resources” will be 10%.

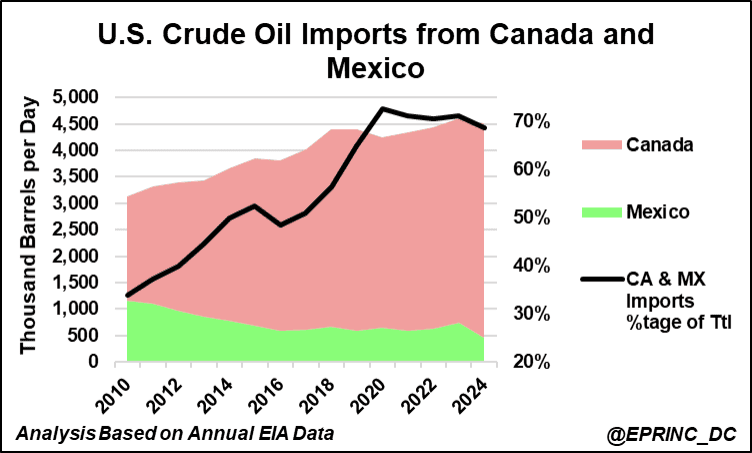

At 4 million barrels per day (MBD) and 0.5 MBD, respectively, Canada and Mexico have risen in recent years to account for approximately 70% of total U.S. crude oil imports (6.5 MBD) (Figure 1). Other U.S. crude oil imports from countries such as Saudi Arabia and Nigeria have declined accordingly.

Canadian imports are generally priced at a discount of $14 per barrel against the U.S. benchmark price of West Texas Intermediate (WTI) while the discount on Mexican imports is approximately $5. Using these metrics, the total implied annual value of Canadian and Mexican imports was $104 billion in 2024 ($92 billion for Canada; $12 billion for Mexico). This is about 12% of the entire trade ($900 billion) with Canada and Mexico.

Of total U.S. crude oil consumption, Canadian and Mexican imports account for almost 30%. Applying the stated tariff rates in President Trump’s EOs, the implied annual increase to the cost of Canadian and Mexican imports would be an additional $10.4 billion, or 2.9%.

Since crude oil costs are passed on to product prices, this would imply, in the aggregate, an increase of 9 cents per gallon using the current U.S. national average of $3 for regular gasoline.

Crude quality matters: while the U.S. produces a considerable amount of crude oil, U.S. refiners have been reliant for a long time on the types of medium and heavy sour (sulfuric) crudes available from Canada and Mexico because they can run their refineries more profitably. Alternative sources that can only partially replace Canadian and Mexican resources would be from Venezuela (currently limited due to sanctions), Kuwait, and Saudi Arabia.

Background:

On December 8, 1993, NAFTA (the North American Free Trade Act) was signed into law. The signatories were Canada, Mexico, and the U.S. NAFTA sought to ease trade restrictions, increase commercial investment, and develop dispute resolution mechanisms. Since NAFTA’s ratification, merchandise trade between the member countries has doubled.

On September 30, 2018, a new agreement was ratified adjusting key terms and renamed to USMCA (U.S., Mexico, Canada Agreement). Over the course of more than thirty years, NAFTA/USMCA has transformed the countries of North America into an integrated energy and industrial region leading to increased intraregional and interregional production and trade.

The unilateral and sudden implementation of tariffs creates considerable negative shocks to the existing complex interdependent systems impeding flows and increasing costs.

Key Links:

- Executive Order—”Imposing Duties to Address the Flow of Illicit Drugs Across Our Northern Border” https://www.presidency.ucsb.edu/documents/executive-order-imposing-duties-address-the-flow-illicit-drugs-across-our-northern-border

- Executive Order—”Imposing Duties to Address the Situation at Our Southern Border” https://www.presidency.ucsb.edu/documents/executive-order-imposing-duties-address-the-situation-our-southern-border

- Executive Order—”Imposing Duties to Address the Synthetic Opioid Supply Chain in the People’s Republic of China” https://www.presidency.ucsb.edu/documents/executive-order-imposing-duties-address-the-synthetic-opioid-supply-chain-the-peoples

- White House Fact Sheet: “President Donald J. Trump Imposes Tariffs on Imports from Canada, Mexico and China” https://www.whitehouse.gov/fact-sheets/2025/02/fact-sheet-president-donald-j-trump-imposes-

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “The Cost Impact of President Trump’s Tariffs on U.S. Crude Oil Imports from Canada and Mexico: A First Assessment,” Chart of the Week 2025-06, February 3, 2025.