On June 22, 2025, the Iranian parliament authorized the blocking of the Strait of Hormuz in retaliation for a series of increasingly aggressive military exchanges with Israel and the United States that culminated in airstrikes on Iran’s nuclear enrichment facilities and military installations during the prior week. The Strait is critical to the shipment of crude oil and petroleum product exports ranging up to 20 million barrels per day, along with large volumes of LNG shipped primarily from Qatar.

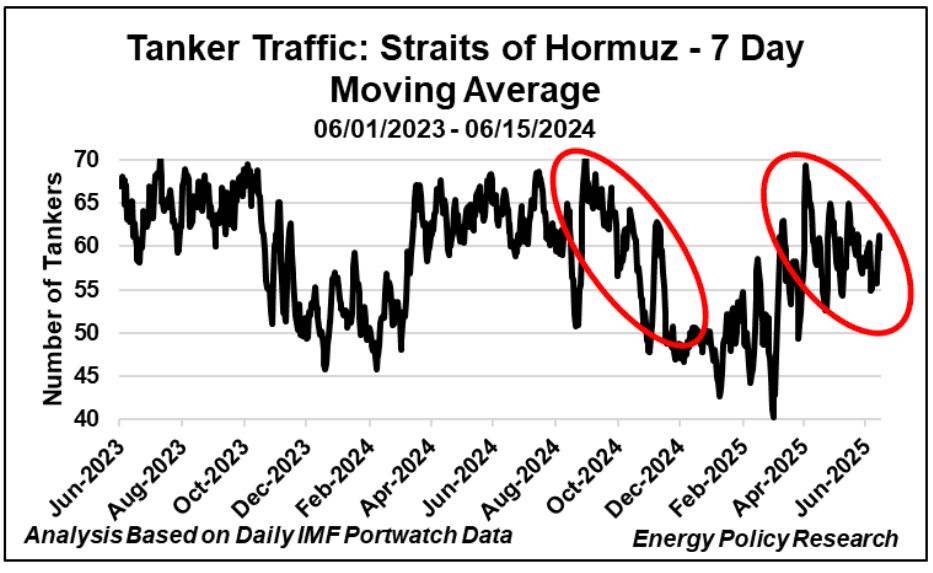

Tanker traffic through the Strait follows seasonal patterns, with lower transits from October through April. Increased military maneuvers in the region curtailed peak seasonal traffic sooner in late 2024. Traffic recovered somewhat at the start of 2025 but has begun to fall off again in recent months. News services report some withdrawal of crews by major integrated oil companies from regional oil fields and production facilities, as well as uncertainty among tankers about crossing the Strait. Vessel tracking sites such as marinetraffic.com and vesselfinder.com show traffic continuing, but with large clusters of tankers loitering just outside the Strait and to the south of the coast of Fujairah, the second largest bunkering port in the world.

A closure by military force would be difficult to sustain. To close the Strait, Iran would need to occupy and control Oman’s side, through which most vessels transit. Doing so would immediately invoke the defense pact of the Gulf Cooperation Council (GCC), a regional economic, political, and military union of Arab Gulf states that includes Oman but excludes Iran.

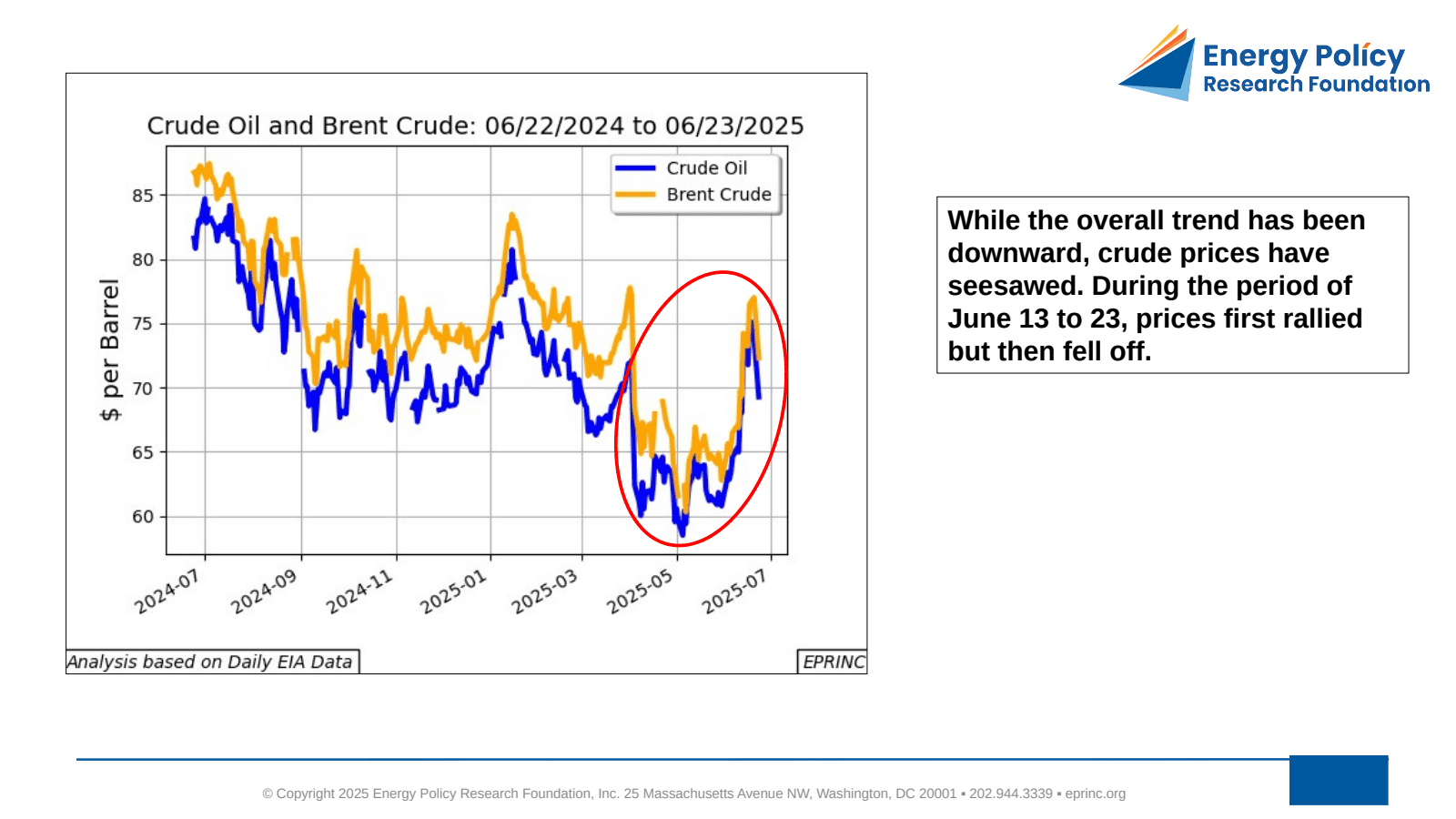

While the overall trend in crude prices has been downward, prices have seesawed. Over the period of June 13 to 23, benchmark prices first rallied and then fell off.

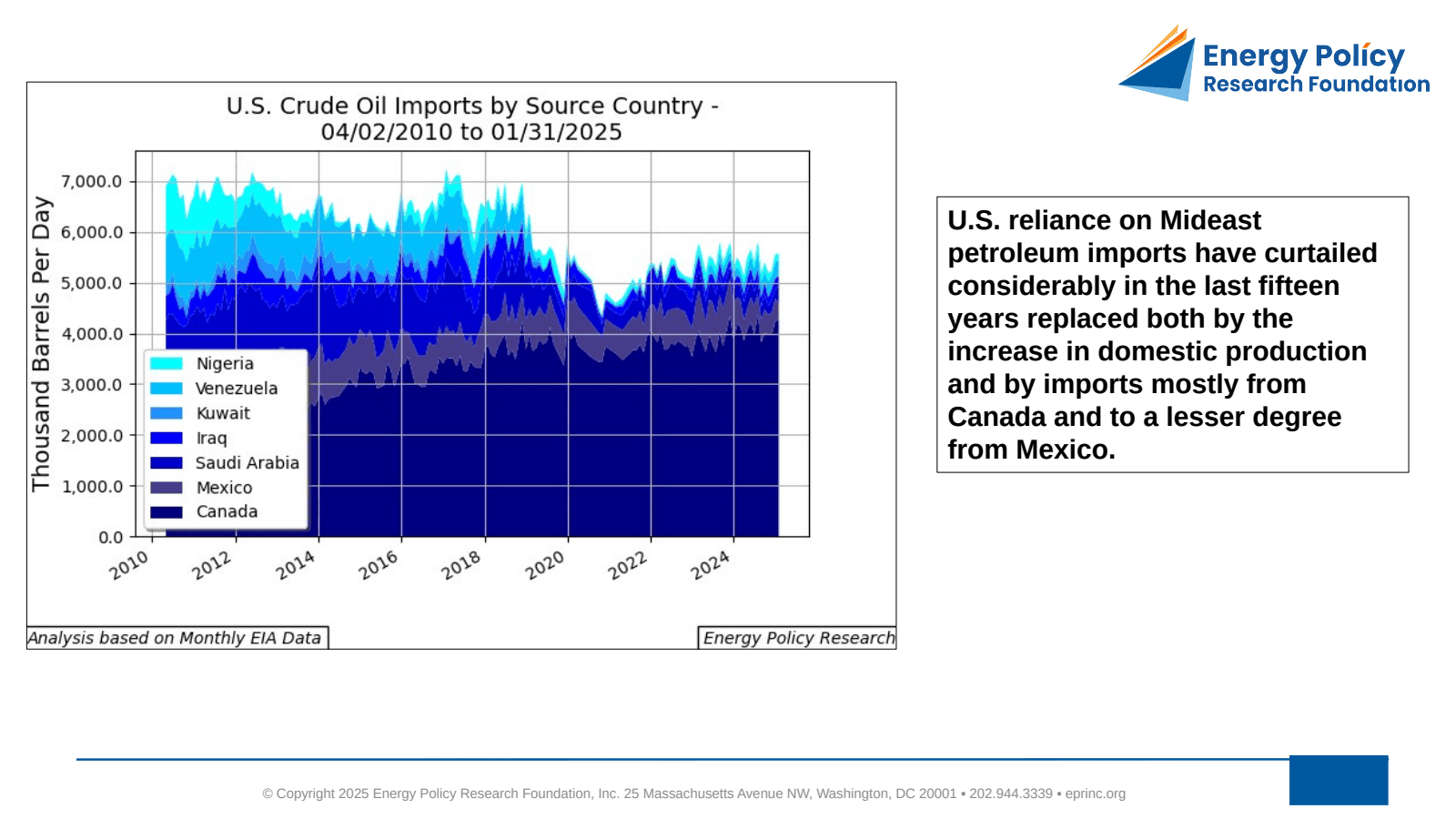

U.S. exposure to any disruption has narrowed considerably. Reliance on Mideast petroleum imports has curtailed sharply over the past fifteen years, replaced both by increased domestic production and by imports mostly from Canada and, to a lesser degree, Mexico.

From the EPRINC Chart of the Week archive.

Cite: EPRINC, “Mideast Military Aggression, Hormuz Strait Tanker Traffic, and Crude Oil Prices,” Chart of the Week 2025-25, June 16, 2025.