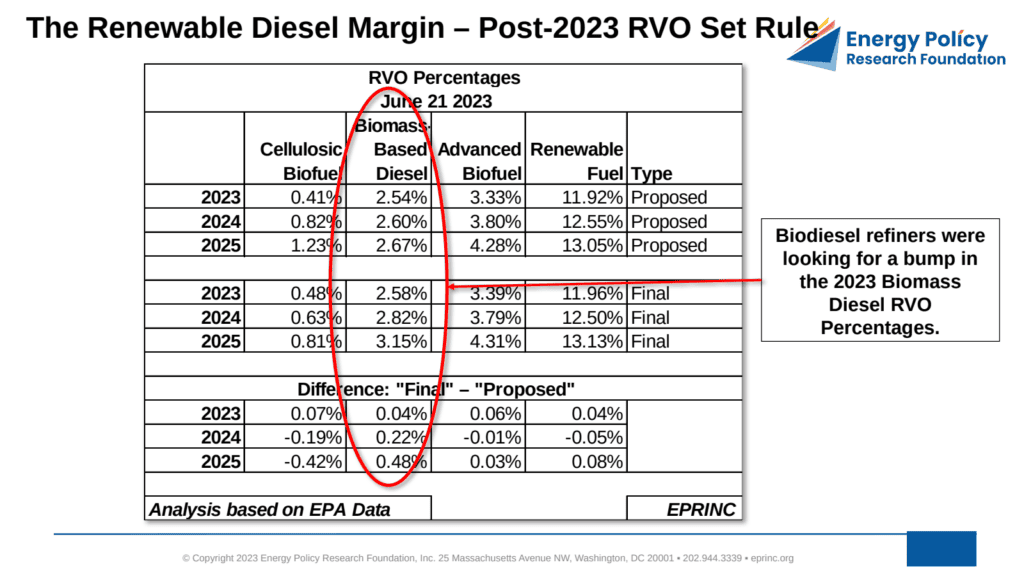

EPA released its post-2023 Renewable Fuel Standard (RFS) Renewable Volume Obligations (RVO) final “set” rule on June 21, 2023. Renewable diesel refiners had anticipated an increase in the 2023 biomass diesel RVO percentages but did not receive one. Following the announcement, the renewable diesel margin collapsed.

The margin is built from four components. It captures the value of the finished fuel and its associated credits against the cost of feedstock, using the following formula:

NYMEX ULSD + (1.7 × Biodiesel RIN) + (0.00707 × LCFS Credit) − (8.5 × CBOT Soybean Oil), where the inputs are the New York ultra-low-sulfur diesel price ($/gallon); the D4 biodiesel RIN price ($/RIN, converted at 1.7 D6 ethanol RINs); the California Low Carbon Fuel Standard (LCFS) credit ($/metric ton, with renewable diesel at a carbon intensity of 54 earning 0.00707 of a credit per gallon); and the Chicago soybean oil price ($/pound, with 8.5 pounds required to produce one gallon of renewable diesel).

Both sides of the equation moved against producers. Soybean oil, a key input, has surged on tight supply and demand balances and uncertainty over the availability of Ukrainian shipments. At the same time, D4 biomass diesel RIN prices dropped in response to the unexpectedly low biomass diesel RVOs in the final rule.

Renewable diesel production is valued as a generator of D4 biomass diesel RINs and California LCFS credits. By declining to raise the 2023 biomass diesel obligation, EPA weakened one of the principal credit revenue streams underpinning renewable diesel economics, squeezing margins even as feedstock costs stayed high.

From the EPRINC Chart of the Week archive.