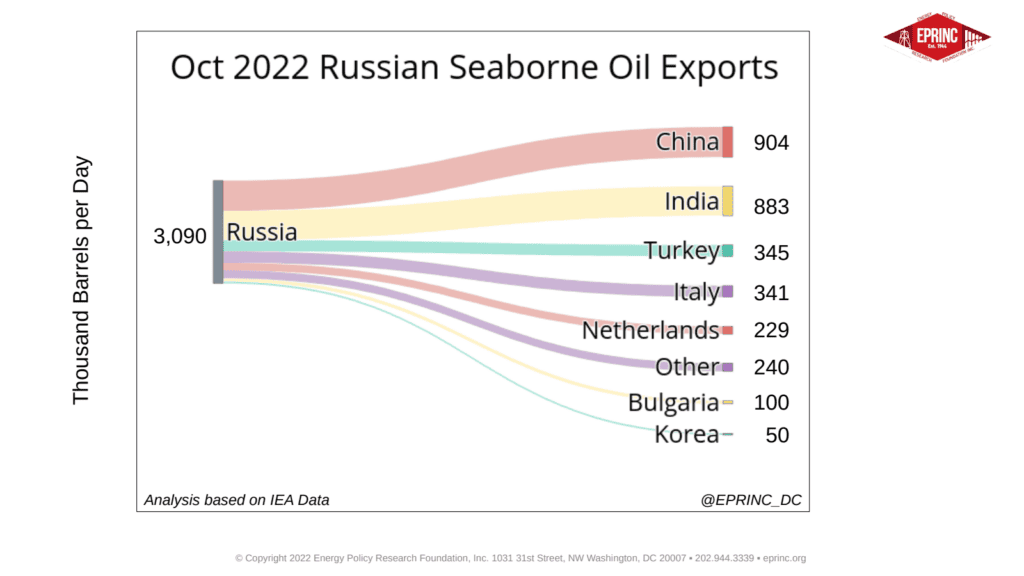

Russia produces an estimated 10.8 million barrels per day (MB/d) of crude oil, of which about 3.5 MB/d moves by ocean-going vessel, primarily to Asia and European Mediterranean countries, with a small balance to the Americas. Market consultancies estimate these seaborne exports require roughly 240 vessels of varying capacities—mostly Aframaxes and Suezmaxes carrying 650 to 900 thousand barrels, with some VLCCs capable of moving about 2 million barrels. Russia controls only about 60 of those vessels, or 25% of the count but only 21% of total capacity. With its current account surplus expected to reach $265 billion in 2022, second only to China’s, members of the G7, EU, and Australia have sought constraints on Russia’s petroleum trade that would reduce Kremlin revenues while minimizing disruption to global oil flows.

Because embargos and import tariffs risk supply shocks and inflationary price impacts against a background of global inflation and potential recession, policymakers turned to a price cap. In September 2022, the EU’s Trade, Technology, and Energy Council formalized proposals for a cap on all Russian seaborne petroleum trade, and the U.S. Department of Treasury’s Office of Foreign Assets Control announced similar measures. The cap on crude took effect December 5, 2022, with the cap on petroleum products to follow February 5, 2023.

- Mechanism: a price set below prevailing global benchmarks but above production costs, kept at a minimum 5% below market rates and reviewed every two months, with the IEA advising on appropriate levels. Vessels loaded with Russian crude before December 5, 2022 had until January 19, 2023 to unload—an effective 45-day transition.

- Enforcement: maritime insurers. G7 countries control 90-95% of the global shipping insurance market, placing most of the Russian oil trade within G7 jurisdiction.

- Penalties: vessels deemed out of compliance face a 90-day prohibition on maritime insurance, financing, and servicing, with stricter penalties for EU vessels subject to EU legislation.

The cap was announced at $60/bbl on December 2, 2022. On that date, Russian Urals crude was trading at $48/bbl at St. Petersburg, well below the cap. In response, the Kremlin announced a draft presidential decree barring sales to any party participating in the mechanism, and has sought to expand a shadow fleet: since February 2022, some 66 vessels aged 15 years or older have transferred to entities assumed to be Russian—still nearly 50% short of the capacity needed to move all exports, and drawn largely from a limited pool already used to carry sanctioned Iranian and Venezuelan oil. Ukraine’s President Zelensky objected to the cap’s leniency, praising Poland and the Baltic states for urging tougher action, while OPEC, meeting December 4, resolved to hold existing quotas without citing the cap.

The mechanism aspires to strengthen the realignment of flows already underway since February 2022, rerouting Russian crude from Europe to China, India, Turkey, and Southeast Asia, and could degrade seaborne exports by 1.5 MB/d by the end of the first quarter of 2023. A potential unintended consequence is over-compliance: given the extensive documentation required by G7 and EU regulators, some shipping companies’ legal counsel may judge the risks too great and decline to move Russian cargos at all.

From the EPRINC Chart of the Week archive.