Recent winters across the northern latitudes have been harsh. This has elevated reliance on natural gas for additional seasonal power and heating in both the U.S. and Europe.

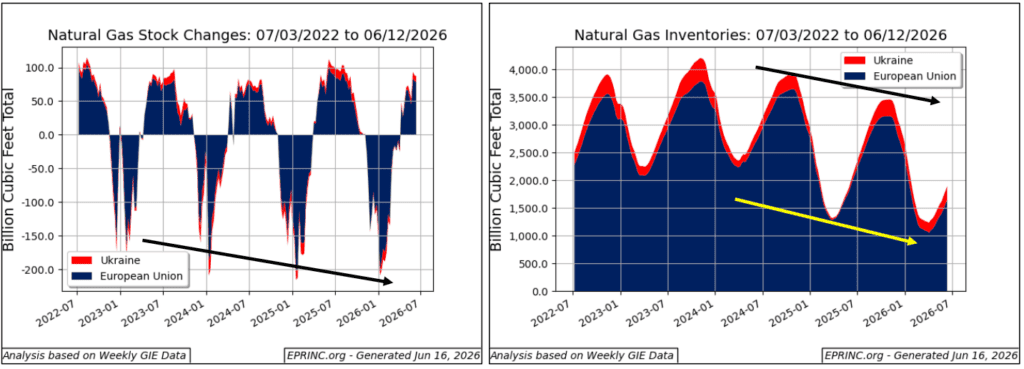

Europe and Ukraine have a combined 5 trillion cubic feet (tcf) of storage (4 tcf in Europe, 1 tcf in Ukraine). In recent years, Ukraine’s storage capacity has been used to support the rest of Europe’s; however, Russia’s military aggression has curtailed its utilization to half.

Mid-year European natural gas replenishments peaked in November 2023 at 4.2 tcf (3.8 tcf in Europe and 0.42 in Ukraine) and have not attained similar levels since. Winter inventory depletions are on track to continue to reach new lows, requiring more aggressive replenishments.

European sanctions policy against Russia, failure to renew pipeline transit agreements, and other things have caused Europe to shift from a situation where the majority of natural gas imports were transited via international pipelines to one where the majority is moved as LNG (and since mid-2022 the bulk of that Europe-bound LNG is coming from the U.S.). In the event European winters continue to be severe, seasonal heating challenges might arise.

European Natural Gas Inventories — Mid-2026 Assessment

Winters in the U.S. have been similar to those in Europe, increasing in intensity in the last several seasons. This has caused natural gas inventory weekly depletions to increase, with those in February 2026 reaching as high as 300 billion cubic feet (bcf).

Despite these aggressive drawdowns, U.S. natural gas production resilience has restored levels to 4 tcf ahead of each heating season. Inventories appear to be on track to reach similar levels this year.

From the EPRINC Chart of the Week archive.