The Hormuz Strait blockade brought on by the ongoing war between Israel / the U.S. and Iran has created the largest energy supply shock ever. It has led to shortages and price spikes in hydrocarbon commodities, fertilizer, and helium.

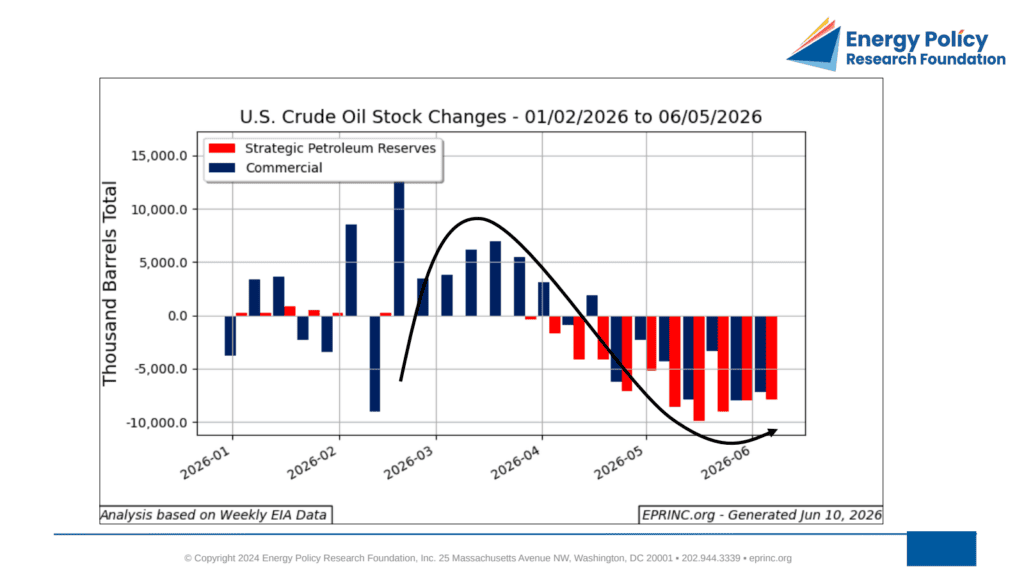

U.S. crude oil inventories declined from 855 million barrels at the end of February 2026 to 776 million barrels by June 5, 2026, with the Strategic Petroleum Reserve falling 65 million barrels to 350 million and commercial stocks declining 14 million barrels to 426 million. These drawdowns occurred as part of an IEA-coordinated release of 400 million barrels across 32 OECD countries over 120 days, of which the U.S. committed 172 million barrels.

The singular critical multinational relief effort has been coordinated by the International Energy Agency (IEA). On March 11, 2026, the IEA announced the release of 400 million barrels (MBs) of strategic crude oil inventories held by 32 OECD countries for a period of 120 days, implying a rate of 3.3 MB/d. The U.S. has committed to 172 MBs of this total.

At the onset of the crisis at the end of February, the U.S. held a total of 855 MBs of crude oil in storage (of which 440 MBs were commercial and 415 MBs were in the Strategic Petroleum Reserve – SPR). As of June 5, 2026, commercial inventories have declined by 14 MBs to 426 while the SPR stood at 350 MBs, down 65 MBs based on data published by EIA on June 10, 2026.

While this has muted price spikes and shortages, the IEA, trading companies, and analysts are warning of adverse conditions within the next few months if Hormuz commodity flows are not restored soon.

Numerous efforts to mitigate the adverse effects of the shock have been put in place; the substantive ones include diversion of crude oil supplies via pipeline across the Arabian peninsula to the Red Sea, the temporary waiver of the U.S. Jones Act through August 16, 2026 lowering U.S. maritime costs, China’s drastic reduction of crude oil imports favoring domestic reserves, and the drawing down floating storage.

For more information on these charts, please contact Max Pyziur (maxp@eprinc.org)

From the EPRINC Chart of the Week archive.