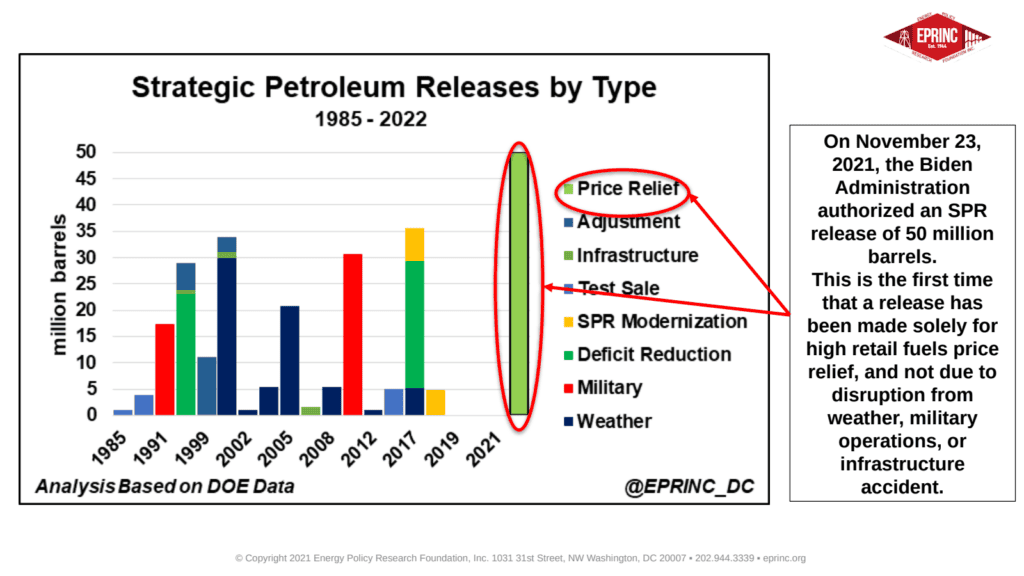

Over the course of 2021, U.S. transportation fuel prices climbed steeply to levels not seen in almost a decade, rising roughly 40% at the national level from the beginning of 2020 through the most recent period. In response, the Biden administration announced on November 23, 2021 the release of 50 million barrels (MBs) from the U.S. Strategic Petroleum Reserve (SPR) — the equivalent of three to four days of U.S. consumption — and concurrently requested that the FTC investigate whether “illegal conduct is costing families at the pump.” The release was coordinated with China, India, Japan, and Korea, but outside the auspices of the International Energy Agency (IEA), which traditionally coordinates strategic stock releases on behalf of OECD member countries.

The SPR was established in the 1970s in reaction to oil supply shortages brought on by political instability in Middle East producing countries. Its anticipated use has been to counter supply disruptions from events such as extreme weather, military conflicts, geopolitically motivated embargos, and major infrastructure accidents, typically undertaken in conjunction with other OECD countries under IEA oversight. None of these conditions is currently impairing petroleum production, trade, and distribution. The June 2011 Obama administration release of 30.7 MB, in response to the Libyan Civil War, was the highest previous release and was part of an IEA curtailment action. While previous administrations have considered using the SPR for price relief, this is the first explicit instance of a release without a concurrent supply disruption threat or occurrence.

The administration has been criticized for pursuing this release alongside policies likely to constrain U.S. oil and gas production, among them the earlier cancellation of the Keystone XL Pipeline and the suspension of the federal oil and gas lease sale program.

EPRINC’s research and discussions with practitioners indicate that rising prices are attributable to four sets of structural factors adding frictions across the petroleum product supply chain:

- Upstream investment: exploration and production spending has flattened considerably, with new discoveries replacing only about a third of demand at current consumption levels (see EPRINC Chart of the Week 33).

- Capital availability: financing for E&P companies has become constrained, with private equity now the primary source as public equity markets have lapsed and underwriters have grown more selective in seeking returns.

- Refining feedstock and renewable mandates: high corn prices pass through to ethanol prices and on to consumers, while high renewable energy mandates against constrained demand have driven up prices for renewable energy credits (see EPRINC Chart of the Week 11).

- Distribution and retail: gasoline stations — mostly owned by individuals or specialized distributors rather than oil companies — face shortages of station employees and truck drivers and rising operating costs; fewer drivers mean truckload deliveries are missed more frequently, leading to run-outs at filling stations.

Because the current price increase reflects these structural constraints rather than an acute supply emergency, a strategic stock release of a few days’ consumption addresses none of the underlying causes.

From the EPRINC Chart of the Week archive.