The U.S. crude oil export ban—enacted in 1975 in response to shortages brought on by the October 1973 Arab Oil Embargo—was lifted in December 2015, on the heels of the surge in U.S. hydrocarbon production during the late 2000s. Since then, U.S. crude oil exports have grown to over 4 million barrels per day (MB/d). Europe, including Türkiye, imports approximately 1.4 MB/d of that total, ranging between 35% and 42%.

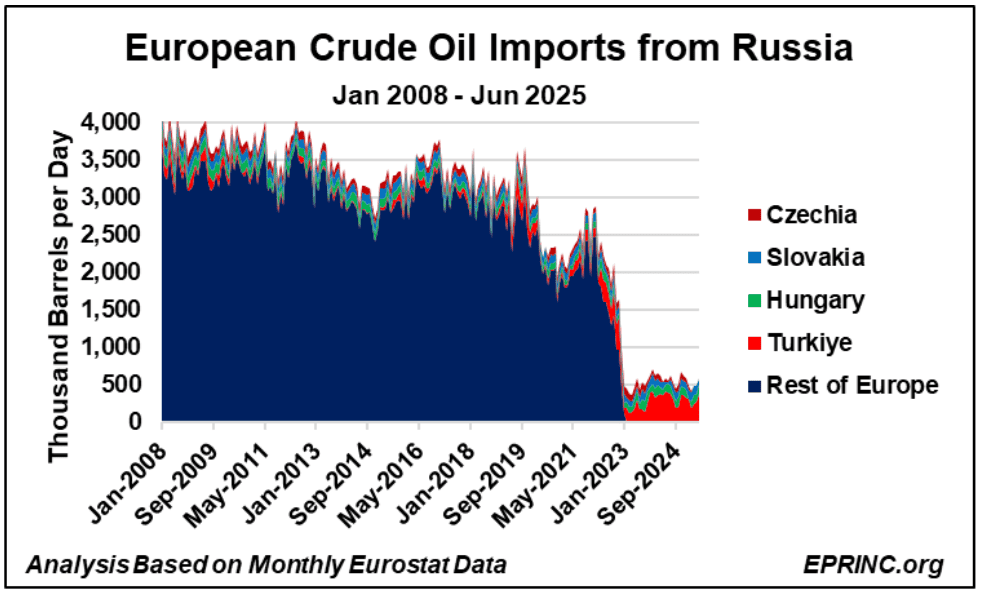

European crude oil imports held steady at approximately 9 MB/d until 2020 but have declined to 7.5 MB/d since then. These imports are sourced from OPEC-Africa (Algeria, Libya, Nigeria), OPEC-MidEast (Iraq, Saudi Arabia, Kuwait, United Arab Emirates), Central Asia (Azerbaijan, Kazakhstan), and Other Americas (Canada, Mexico, Brazil, Venezuela). Through 2022, Russian crude oil supplied between 3 and 4.5 MB/d—40% to 50% of the total.

Following the escalation of Russia’s war against Ukraine in 2022 and the sanctions imposed in response, Russian crude oil imports have been curtailed to an average of 540 thousand barrels per day (TB/d) since January 2023. The remaining volumes flow primarily to Türkiye (averaging 288 TB/d), Hungary (96 TB/d), Slovakia (91 TB/d), and Czechia (61 TB/d).

On July 28, 2025, the Trump administration concluded a nonbinding framework agreement for the EU to purchase $750 billion of U.S. energy over three years, or $250 billion per year. In the trailing twelve months through June 2025, U.S. crude oil exports were valued at $101 billion, of which exports to Europe accounted for $32 billion (32.5%). Replacing the residual 540 TB/d of Russian crude imports with U.S. barrels would have raised the value of U.S. crude exports to Europe to $44 billion, an increase of $12 billion.

From the EPRINC Chart of the Week archive.