Under U.S. law, the Renewable Fuel Standard (RFS) requires refiners and importers to blend specific volumes of biofuels into transportation fuels. Compliance is met by acquiring and submitting Renewable fuel Identification Numbers (RINs), the credits generated when biofuels are produced or blended. Because the RFS carries discretionary policy components that can range from lax to aggressive, the effective stringency of the mandate shifts with whichever administration is in power.

RIN prices for the principal categories (D4, D5, D6) are driven largely by the generation and retirement of the credits. Since January 2025, more aggressive policy has tightened RIN supplies, and prices have doubled as a result.

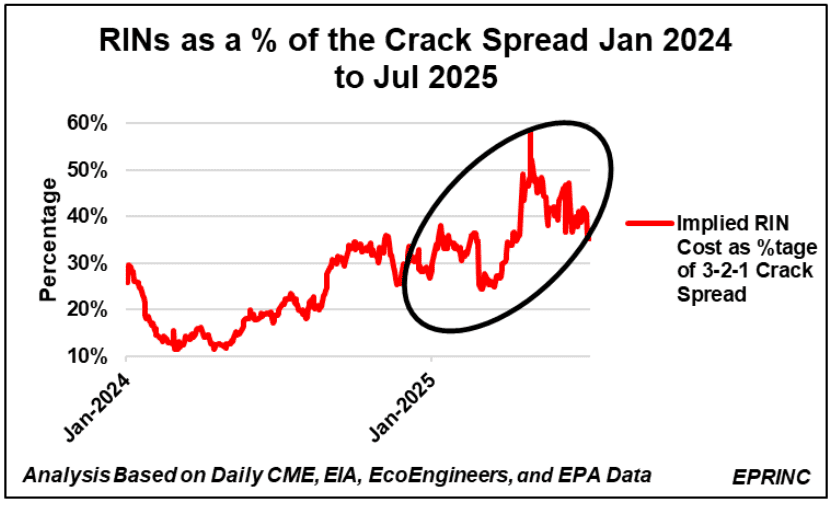

A simple gauge of refiner margins is the 3-2-1 crack spread, computed by summing the price of two barrels of gasoline and one barrel of diesel and subtracting the cost of three barrels of crude oil. Since the start of 2025, the crack has trended upward from roughly $17/bbl to $24/bbl.

The question is how much of that margin is claimed by RFS compliance. Using EPA volumetric requirements and other metrics, EPRINC estimates that over the course of 2025 the RFS claim on the crack spread rose from 30% to 40%, spiking to nearly 60% at one point. The rising cost of compliance underscores how discretionary policy choices translate directly into refiners’ economics.

From the EPRINC Chart of the Week archive.