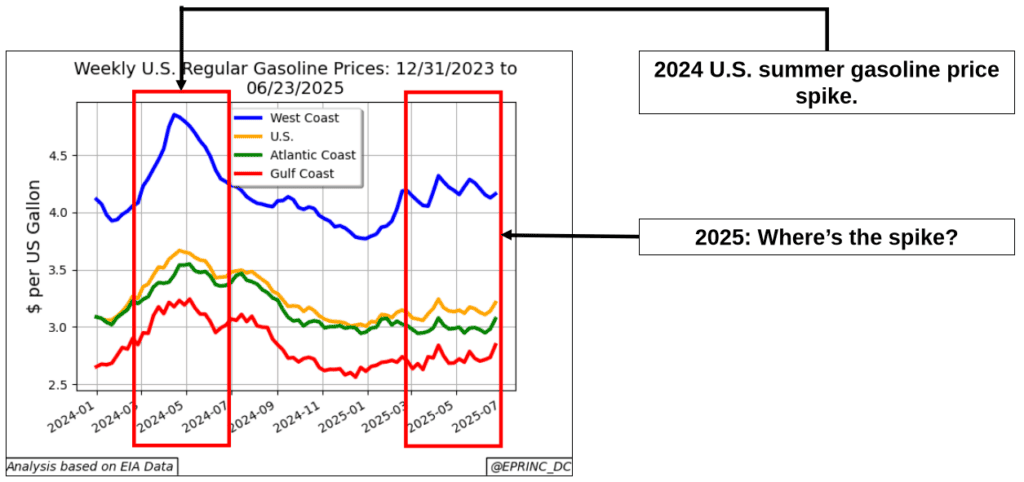

WASHINGTON/NEW YORK, July 9, 2025 – U.S. gasoline prices generally rise substantially with the onset of the summer driving season. However, except for California and the other West Coast states, prices have been generally flat during the summer of 2025, a distinct deviation from historical trends (Figure 1).

This is even more surprising given that in the current context demand has not slackened; VMTs (vehicle miles traveled) continue their upward trend (EPRINC Chart of the Week 2025-04 – VMTs vs U.S. Gasoline Sales), albeit with improving efficiency, and there are several risk factors that could lead to tight supplies.

The risk factors include:

- declines in Hormuz Strait tanker traffic coupled with the threat of the Strait’s closure by Iranian military aggression (EPRINC Chart of the Week 2025-25 – Tanker Traffic Through the Hormuz);

- record-high but flattening of U.S. crude oil production due to prices dropping below breakeven levels (EPRINC Chart of the Week 2025-14 – Dallas Fed: U.S. Crude Oil Production Costs are Rising); and

- crude oil and product inventories at levels considerably below the 5-year average.

Some price relief is imminent with the recently announced OPEC+ August 2025 production increase.

N.B.: West Coast gasoline prices are dominated by California. California has gasoline standards and regulations that far exceed any found in the rest of the U.S. Their goal is to mitigate ozone-causing pollution and GHG emissions. As a consequence, California transportation fuels are only produced by in-state refineries at considerable expense, costs that are passed on to consumers at higher prices (please see EPRINC Policy Briefing – Understanding California’s High Transportation Fuel Prices).

From the EPRINC Chart of the Week archive.