On February 1, 2025, President Donald Trump issued three Executive Orders applying tariffs to all imported goods from Canada, Mexico, and China, with the stated rationale of taking punitive action against the flow of illegal drugs and their components. The tariffs were set at 25% on the value of imported goods from Mexico and Canada and 10% from China, with a key exception setting the rate on Canadian “energy and energy resources” at 10%. Originally slated to take effect February 4, the tariffs on Canadian and Mexican goods were postponed for a month pending further deliberations.

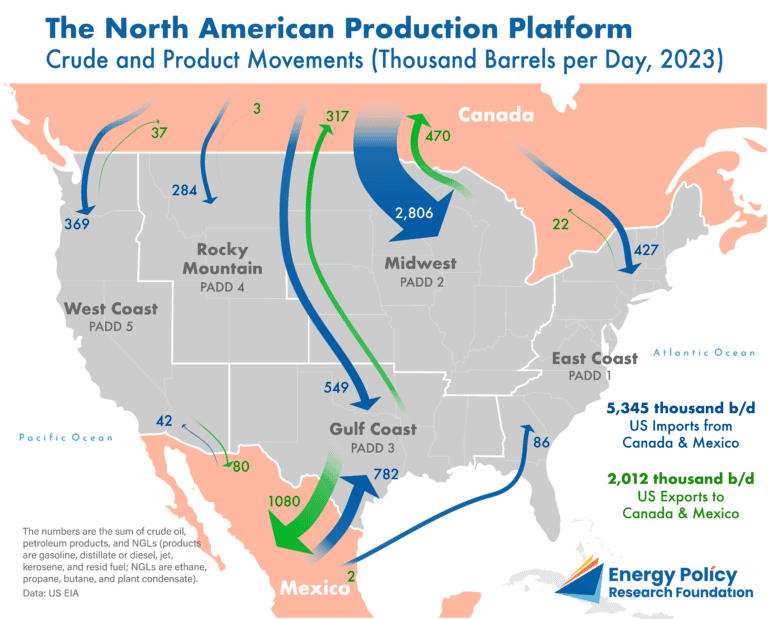

The chart traces the crude oil and product movements that bind together the North American production platform. Canada ships 2,800 thousand barrels per day (TBD) of crude into the U.S. Midwest, and Mexico ships 780 TBD into the U.S. Gulf Coast. The quality of these crude oils is critical to the refinery fleets in these regions, allowing them to operate efficiently and remain commercially sustainable.

The trade runs in both directions. Much of the distillate (diesel) and propane produced in the U.S. in excess of domestic needs is shipped primarily to Canada and Mexico—780 TBD and 1,080 TBD, respectively—and is integral to those markets. Other U.S. regions, including the Northwest and the Atlantic Coast, also benefit from the synergies of crude oil and products produced and traded across the continent.

“If there is no resolution to the issues, the proposed tariffs on Canadian and Mexican oil and refined products will be counter-productive,” said Batt Odgerel, EPRINC’s Director for Energy Transition Research. “It will cause prices to rise and will undermine energy security in all three countries.”

From the EPRINC Chart of the Week archive.