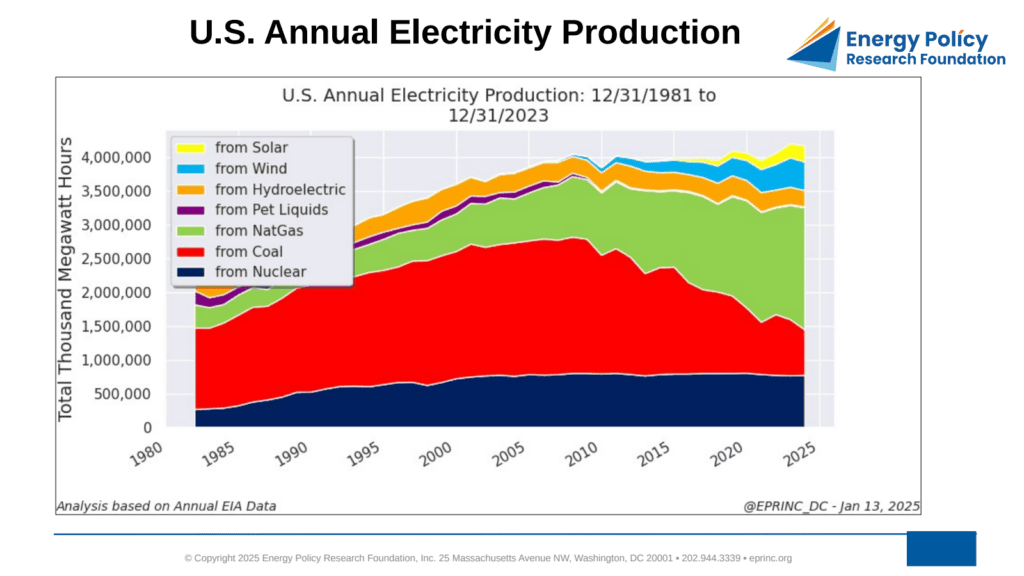

The chart tracks total U.S. electricity production and residential electricity prices over the long run. Between 1981 and 2002, production grew at an annual rate of 2.4%, rising from 2.3 trillion kilowatt hours (kWh) to 3.76 trillion kWh. From 2003 to 2023, growth slowed to just 0.5% per year, reaching 4.17 trillion kWh in 2023. Beginning in 1992, energy efficiency mandates and incentives—most notably the Energy Star program administered by the EPA and other agencies—allowed consumers to increase their use of appliances, lighting, and electronics while overall electricity requirements remained flat.

The generation mix has changed substantially over the period. Through 2003, coal was the dominant resource at over 52% of total generation, with nuclear and natural gas distant seconds at 17.5% and 14.1%, respectively. The combination of hydraulic fracturing and lateral drilling, which came into full use in the late 2000s, produced a bounty of inexpensive natural gas, while greenhouse gas reduction mandates—known as renewable portfolio standards (RPS)—reduced or in some jurisdictions eliminated coal-fired power. Coal now accounts for 16.2% of total generation and natural gas for 43.3%. RPS policies also spurred solar and wind, which reached 5.7% and 10% of total generation, respectively, in 2023.

Although demand has been flat overall since 2003, residential prices have varied widely across jurisdictions. California, with the most aggressive statewide RPS, has seen the largest increases in U.S. residential electricity prices. Texas enacted an RPS in 1999 and makes extensive use of production tax credits favoring wind, yet its residential prices have remained generally flat and low; state authorities have largely integrated wind’s intermittency with dispatchable generation, though extreme cold and hot weather have at times led to extensive blackouts.

Despite decades of efficiency gains, forecasters anticipate rising power needs driven by electric vehicles, electrification of residential and commercial heating, and the growing use of power-intensive generative artificial intelligence. The magnitude remains uncertain, but forecasts point to a distinct upward shift from the demand pattern of the last twenty years.

From the EPRINC Chart of the Week archive.