After the shortages and price spikes of 2022, European countries built natural gas inventories aggressively throughout 2023. At the beginning of November 2023, EU storage reached 3.785 trillion cubic feet, or 224 billion cubic feet (6.3%) more than the prior year. During November through early December, however, most of Europe experienced a cold wave; as measured by heating degree days, temperatures were 14.1% lower than the prior year. Over that period Europe depleted 315 BCF of storage, 31% more than in 2022.

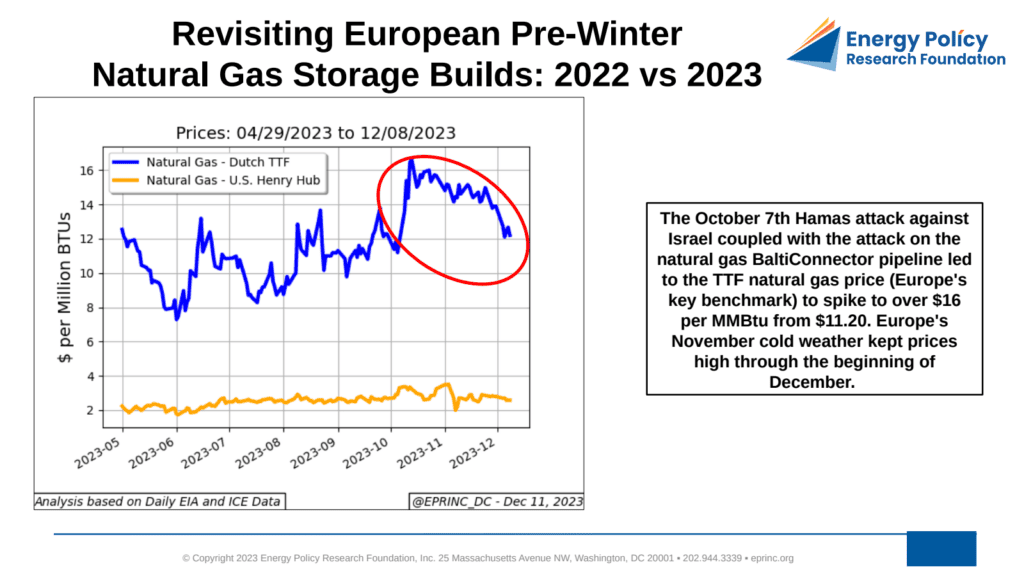

Prices reflected the tighter conditions. The October 7th Hamas attack against Israel, together with the attack on the Balticonnector natural gas pipeline, drove the TTF benchmark — Europe’s key natural gas price — from $11.20 to over $16 per MMBtu. November’s cold weather kept prices elevated through early December.

Demand-side measures continued to cushion the market. Aggregate natural gas consumption across Western Europe (the Netherlands, Belgium, France, Germany, Italy, and the United Kingdom) typically peaks in January at close to 55 BCF/d. In January 2023, mild weather and efficiency measures held the peak to just over 40 BCF/d, some 15 BCF/d below average highs.

Imports remain central to Europe’s winter energy security, sourced via pipeline and, more importantly, LNG. In early 2023, European natural gas imports peaked at over 20 BCF/d, with 13 to 14 BCF/d of that in the form of LNG. Following Russia’s 2022 aggression against Ukraine and a series of reciprocating steps that curtailed Russian pipeline flows to 1 BCF/d, Europe has relied on imports from Africa alongside U.S., Qatari, and other LNG sources.

From the EPRINC Chart of the Week archive.